Deck 6: Portfolio Theory

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Stock A has an expected return of 10% and a standard deviation of 10%.Stock B has an expected return of 15% and a standard deviation of 20%.The two stocks are perfectly negatively correlated (  = -1).What set of weights yields a portfolio with a zero variance?

= -1).What set of weights yields a portfolio with a zero variance?

A) 2/3 in Stock A; 1/3 in Stock B

B) 2/3 in Stock B; 1/3 in Stock A

C) 2 in Stock A; -1 in Stock B

D) 2 in Stock B; -1 in Stock A

E) None of the above.

= -1).What set of weights yields a portfolio with a zero variance?A) 2/3 in Stock A; 1/3 in Stock B

B) 2/3 in Stock B; 1/3 in Stock A

C) 2 in Stock A; -1 in Stock B

D) 2 in Stock B; -1 in Stock A

E) None of the above.

Question

Delilah Jones has a portfolio of stocks A and B.See the table below for details.What is the correlation between the two stocks?

A) -1.0

B) -0.5

C) 0

D) 0.5

E) 1.0

A) -1.0

B) -0.5

C) 0

D) 0.5

E) 1.0

Question

Stocks A and B are perfectly negatively correlated (  = -1)and their standard deviations are 0.20 and 0.30 respectively.What is the standard deviation of a portfolio with 50% invested in Stock A and 50% invested in Stock B?

= -1)and their standard deviations are 0.20 and 0.30 respectively.What is the standard deviation of a portfolio with 50% invested in Stock A and 50% invested in Stock B?

A) 5%

B) 6%

C) 7%

D) 8%

E) 9%

= -1)and their standard deviations are 0.20 and 0.30 respectively.What is the standard deviation of a portfolio with 50% invested in Stock A and 50% invested in Stock B?A) 5%

B) 6%

C) 7%

D) 8%

E) 9%

Question

Question

Question

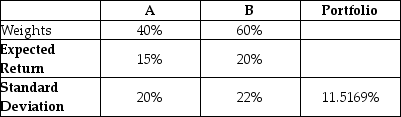

Consider the data provided in the table below for a portfolio of Assets A and B.The correlation of the two assets is ρ = -0.9523.What is the standard deviation of the returns of the portfolio?

A) 6.25%

B) 25%

C) 35%

D) 55%

E) 57.5%

A) 6.25%

B) 25%

C) 35%

D) 55%

E) 57.5%

Question

An investor is considering investing one-half of his wealth in Asset A and one-half in Asset B.He is not sure how the two assets are correlated.The correlation might be r = +1 or it might be r = -1.If it is r = + 1,then the portfolio standard deviation is 15%.Calculate the portfolio standard deviation if the correlation is r = -1.What is the difference between the standard deviations of Scenario 1 and Scenario 2? (Scenario 1 - Scenario 2)

A) 2.5%

B) 5.0%

C) 7.5%

D) 10.0%

E) 15.0%

A) 2.5%

B) 5.0%

C) 7.5%

D) 10.0%

E) 15.0%

Question

Question

Question

Question

Question

Question

Question

Question

Question

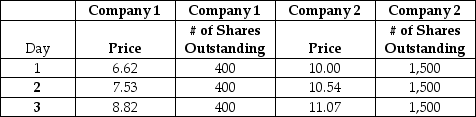

Consider a value-weighted market index that includes the two companies shown in the table.You form a portfolio to mimic the index on Day 1.The mimic portfolio is designed to earn the same return as the index.What is the portfolio weight for Company 1?

A) 15%

B) 16%

C) 17%

D) 18%

E) 19%

A) 15%

B) 16%

C) 17%

D) 18%

E) 19%

Question

Question

Question

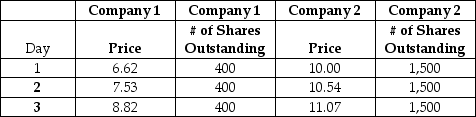

Consider a value-weighted market index that includes the two companies shown in the table.What is the percentage change in the index from Day 1 to Day 2?

A) 4.00%

B) 4.25%

C) 4.50%

D) 4.75%

E) 5.00%

A) 4.00%

B) 4.25%

C) 4.50%

D) 4.75%

E) 5.00%

Question

Question

Question

Question

A popular value-weighted index is constructed out of shares in the two companies,shown in the table below.On Day 1 you construct a portfolio that mimics the index with 15% invested in Company 1 and 85% invested in Company 2.On Day 2,what trades do you need to make in order to adjust your portfolio weights so that your portfolio earns the same return as the index from Day 2 to Day 3?

A) Buy more of Company 1 and buy more of Company 2

B) Buy more of Company 1 and sell some of Company 2

C) Sell some of Company 1 and sell some of Company 2

D) Sell some of Company 1 and buy more of Company 2

E) Make no trades

A) Buy more of Company 1 and buy more of Company 2

B) Buy more of Company 1 and sell some of Company 2

C) Sell some of Company 1 and sell some of Company 2

D) Sell some of Company 1 and buy more of Company 2

E) Make no trades

Question

Question

Question

A popular value-weighted index is constructed out of shares in the two companies shown in the table,below.On Day 1 you construct a portfolio that mimics the index.In order for your portfolio to earn the same return as the index from Day 2 to Day 3,what portfolio weight do you need for Company 1 on Day 2?

A) 12%

B) 13%

C) 14%

D) 15%

E) 16%

A) 12%

B) 13%

C) 14%

D) 15%

E) 16%

Question

Question

Consider a value-weighted market index that includes the following two companies.On Day 1 you form a portfolio to mimic the index.(In other words,to earn the same return as the index.)

What is the portfolio weight on Company 1,and what is the return on the portfolio from Day 1 to Day 2? (Weight %,Return %)

A) 14%, 5%

B) 14%, 6%

C) 15%, 6%

D) 15%, 7%

E) 16%, 5%

What is the portfolio weight on Company 1,and what is the return on the portfolio from Day 1 to Day 2? (Weight %,Return %)

A) 14%, 5%

B) 14%, 6%

C) 15%, 6%

D) 15%, 7%

E) 16%, 5%

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

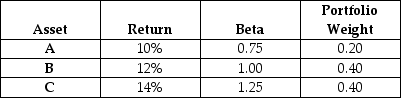

You hold the following portfolio,consisting of Assets A,B and C.What is the portfolio beta?

A) 0.75

B) 1.00

C) 1.05

D) 1.15

E) 1.25

A) 0.75

B) 1.00

C) 1.05

D) 1.15

E) 1.25

Question

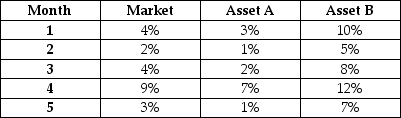

The table below gives the historic return over the past five months for the market portfolio and two assets: A and B.Which of the answers below best describes the historic beta for A and B?

A) βA < 0; βB = 0

B) βA > 0; βB = +1

C) βA > 0; βB = 0

D) βA > +1; βB = 0

E) βA < -1; βB = +1

A) βA < 0; βB = 0

B) βA > 0; βB = +1

C) βA > 0; βB = 0

D) βA > +1; βB = 0

E) βA < -1; βB = +1

Question

Question

Question

Question

Question

Question

Question

Question

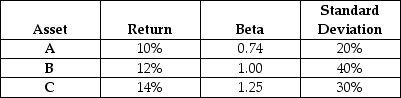

Refer to the data in the table.Which asset possesses the greatest amount of systematic risk?

A) A

B) B

C) C

D) Both A and C

E) Impossible to tell, given the above information

Question

Question

The table below gives the historic return over the past five months for the market portfolio and two assets: A and B.Which of the answers below best describes the historic beta for A and B?

A) βA < 1; βB < 1

B) βA = 0; βB < 1

C) βA = 0; βB > 0

D) βA > 1; βB > 1

E) βA < 1; βB > 1

A) βA < 1; βB < 1

B) βA = 0; βB < 1

C) βA = 0; βB > 0

D) βA > 1; βB > 1

E) βA < 1; βB > 1

Question

Question

Question

Question

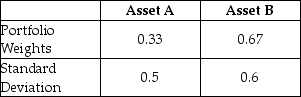

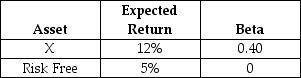

Consider the two assets outlined in the table below.What is the beta of the two asset portfolio given that 40% is invested in X?

A) 0.026

B) 0.085

C) 0.160

D) 0.190

E) 0.220

A) 0.026

B) 0.085

C) 0.160

D) 0.190

E) 0.220

Question

Peter Lynch has the following portfolio of investments:

What is the beta of Peter's portfolio?

A) 1.000

B) 1.126

C) 1.366

D) 1.534

E) 1.877

What is the beta of Peter's portfolio?

A) 1.000

B) 1.126

C) 1.366

D) 1.534

E) 1.877

Question

Question

Question

Question

Question

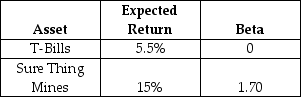

A friend tips you off on a hot stock: Sure Thing Mines Ltd.You only have $10,000 to invest but you want to invest more.Assume that you can borrow an additional $5,000 by short-selling the risk free asset (issuing T-Bills).You purchase $15,000 worth of shares in Sure Thing Mines Ltd.

The expected returns and standard deviations of the two assets are outlined in the table below:

What is the beta of the portfolio?

A) 1.50

B) 1.70

C) 2.50

D) 2.55

E) 2.70

The expected returns and standard deviations of the two assets are outlined in the table below:

What is the beta of the portfolio?

A) 1.50

B) 1.70

C) 2.50

D) 2.55

E) 2.70

Question

Question

Question

Question

Question

Question

Question

Question

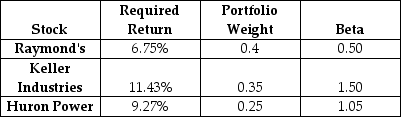

Warren has a portfolio with three stocks as shown in the table.What is the beta of Warren's portfolio?

A) 0.775

B) 0.988

C) 1.017

D) 1.340

E) 1.505

A) 0.775

B) 0.988

C) 1.017

D) 1.340

E) 1.505

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/136

Play

Full screen (f)

Deck 6: Portfolio Theory

1

Can the risk (variance)of a portfolio ever be less than the smallest risk (variance)of an individual security in the portfolio?

A) No. Yes.

B) No. No.

C) Yes. No.

D) Yes. Yes.

A) No. Yes.

B) No. No.

C) Yes. No.

D) Yes. Yes.

No. Yes.

2

Through diversification it is possible to eliminate all of the company-specific risk inherent in owning stocks.However,as a general rule it will not be possible to eliminate systematic (market)risk.

True

3

If two stocks have a correlation of +1,then the standard deviation of a portfolio between them is given by:

σp = wσ1 + (1 - w)σ2

σp = wσ1 + (1 - w)σ2

True

4

________ risk ________ be eliminated through greater diversification and is due to firm-specific or industry-wide factors such as strikes or resource price changes.

A) Systematic; can

B) Systematic; cannot

C) Unsystematic; can

D) Unsystematic; cannot

E) None of the above

A) Systematic; can

B) Systematic; cannot

C) Unsystematic; can

D) Unsystematic; cannot

E) None of the above

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

5

Your broker tells you that it is important to diversify because doing so will increase your expected returns,even if you diversify by randomly selecting stocks (naive diversification).

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

6

You have decided to create a portfolio with two assets: stock X and stock Y.You invest 20% of your funds in X and 80% of your funds in stock Y.The standard deviation of X is 30% and the standard deviation of Y is 40%.The two stocks have a correlation coefficient of - 0.5.What is the portfolio's standard deviation?

A) 30.00%

B) 29.46%

C) 33.24%

D) 36.92%

E) 40.00%

A) 30.00%

B) 29.46%

C) 33.24%

D) 36.92%

E) 40.00%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

7

Answer the following two questions.Assume that the portfolio weights are positive:

1) Can the return on a portfolio ever be less than the smallest return on an individual security in the portfolio?

2) Can the risk (variance) of a portfolio ever be less than the smallest risk (variance) of an individual security in the portfolio?

A) No. Yes.

B) No. No.

C) Yes. No.

D) Yes. Yes.

1) Can the return on a portfolio ever be less than the smallest return on an individual security in the portfolio?

2) Can the risk (variance) of a portfolio ever be less than the smallest risk (variance) of an individual security in the portfolio?

A) No. Yes.

B) No. No.

C) Yes. No.

D) Yes. Yes.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

8

________ risk affects all stocks to a greater or lesser extent and is due to large macroeconomic shocks.This type of risk ________ be eliminated through diversification.

A) Systematic; can

B) Systematic; cannot

C) Unsystematic; can

D) Unsystematic; cannot

E) None of the above

A) Systematic; can

B) Systematic; cannot

C) Unsystematic; can

D) Unsystematic; cannot

E) None of the above

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

9

Which of the following statements is true?

A) A low risk portfolio is constructed by selecting low risk stocks.

B) It is easy to find perfectly negatively correlated stocks.

C) Low risk portfolios will only reflect unsystematic risk.

D) Negatively correlated stocks help build a low risk portfolio.

E) Market risk reduces as more stocks are added to a portfolio.

A) A low risk portfolio is constructed by selecting low risk stocks.

B) It is easy to find perfectly negatively correlated stocks.

C) Low risk portfolios will only reflect unsystematic risk.

D) Negatively correlated stocks help build a low risk portfolio.

E) Market risk reduces as more stocks are added to a portfolio.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

10

You construct an equally weighted,two asset portfolio between ACME Corp.,an American valve and regulator manufacturer,and Wayne Enterprises,a Hong Kong property company.The standard deviation of the returns on ACME's shares is 30% and 55% on Wayne Enterprises.Because of the international diversification,the returns on the two companies have no covariance (correlation = zero).What is the standard deviation of returns of the portfolio?

A) 9.81%

B) 17.60%

C) 22.50%

D) 31.32%

E) 42.50%

A) 9.81%

B) 17.60%

C) 22.50%

D) 31.32%

E) 42.50%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

11

Consider a 2 asset portfolio with 60% in Google Inc.(GOOG)and 40% in John Deere (DE).Google has a standard deviation of 60%,John Deere has a standard deviation of 45% and their correlation is 0.2.What is the standard deviation of returns of the portfolio?

A) 38.33%

B) 43.35%

C) 45.25%

D) 50.00%

E) 52.50%

A) 38.33%

B) 43.35%

C) 45.25%

D) 50.00%

E) 52.50%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

12

Stock A has an expected return of 10% and a standard deviation of 10%.Stock B has an expected return of 15% and a standard deviation of 20%.The two stocks are perfectly negatively correlated ( = -1).What set of weights yields a portfolio with a zero variance?

A) 2/3 in Stock A; 1/3 in Stock B

B) 2/3 in Stock B; 1/3 in Stock A

C) 2 in Stock A; -1 in Stock B

D) 2 in Stock B; -1 in Stock A

E) None of the above.

= -1).What set of weights yields a portfolio with a zero variance?A) 2/3 in Stock A; 1/3 in Stock B

B) 2/3 in Stock B; 1/3 in Stock A

C) 2 in Stock A; -1 in Stock B

D) 2 in Stock B; -1 in Stock A

E) None of the above.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

13

Delilah Jones has a portfolio of stocks A and B.See the table below for details.What is the correlation between the two stocks?

A) -1.0

B) -0.5

C) 0

D) 0.5

E) 1.0

A) -1.0

B) -0.5

C) 0

D) 0.5

E) 1.0

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

14

Stocks A and B are perfectly negatively correlated ( = -1)and their standard deviations are 0.20 and 0.30 respectively.What is the standard deviation of a portfolio with 50% invested in Stock A and 50% invested in Stock B?

A) 5%

B) 6%

C) 7%

D) 8%

E) 9%

= -1)and their standard deviations are 0.20 and 0.30 respectively.What is the standard deviation of a portfolio with 50% invested in Stock A and 50% invested in Stock B?A) 5%

B) 6%

C) 7%

D) 8%

E) 9%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

15

The reason for diversification is to reduce the risk (variance).If the covariance is small (negative)then some portfolios have less variance than any individual securities in the portfolio.Think of the bathing suit and umbrellas company example in the Diversification video.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

16

How would you describe the risk of a company's CEO having a heart attack?

A) Not diversifiable or systematic

B) Not diversifiable or unsystematic

C) Diversifiable or unsystematic

D) Diversifiable or systematic

A) Not diversifiable or systematic

B) Not diversifiable or unsystematic

C) Diversifiable or unsystematic

D) Diversifiable or systematic

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

17

Consider the data provided in the table below for a portfolio of Assets A and B.The correlation of the two assets is ρ = -0.9523.What is the standard deviation of the returns of the portfolio?

A) 6.25%

B) 25%

C) 35%

D) 55%

E) 57.5%

A) 6.25%

B) 25%

C) 35%

D) 55%

E) 57.5%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

18

An investor is considering investing one-half of his wealth in Asset A and one-half in Asset B.He is not sure how the two assets are correlated.The correlation might be r = +1 or it might be r = -1.If it is r = + 1,then the portfolio standard deviation is 15%.Calculate the portfolio standard deviation if the correlation is r = -1.What is the difference between the standard deviations of Scenario 1 and Scenario 2? (Scenario 1 - Scenario 2)

A) 2.5%

B) 5.0%

C) 7.5%

D) 10.0%

E) 15.0%

A) 2.5%

B) 5.0%

C) 7.5%

D) 10.0%

E) 15.0%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

19

Can the return on a portfolio ever be less than the smallest return on an individual security in the portfolio?

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

20

________ is the act of giving something variety.

A) Variance

B) Covariance

C) Deviation

D) Diversification

A) Variance

B) Covariance

C) Deviation

D) Diversification

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

21

An increase in nondiversifiable risk

A) would have no effect on the beta and would, therefore, cause no change in the required return.

B) would cause an increase in the beta and would increase the required return.

C) would cause an increase in the beta and would lower the required return.

D) would cause a decrease in the beta and would, therefore, lower the required rate of return.

A) would have no effect on the beta and would, therefore, cause no change in the required return.

B) would cause an increase in the beta and would increase the required return.

C) would cause an increase in the beta and would lower the required return.

D) would cause a decrease in the beta and would, therefore, lower the required rate of return.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

22

In a well-diversified portfolio,the most relevant type of risk to a well-diversified investor is

A) firm-specific risk.

B) interest rate risk.

C) exchange rate risk.

D) market risk.

E) unsystematic risk.

A) firm-specific risk.

B) interest rate risk.

C) exchange rate risk.

D) market risk.

E) unsystematic risk.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

23

________ is what investors do when they invest equal amounts of money in a portfolio of randomly selected stocks.

A) Naive diversification

B) Efficient investing

C) Sharpe's Method

D) Effective portfolio creation

A) Naive diversification

B) Efficient investing

C) Sharpe's Method

D) Effective portfolio creation

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

24

Risk that affects all firms is called

A) management risk.

B) nondiversifiable risk.

C) diversifiable risk.

D) total risk.

A) management risk.

B) nondiversifiable risk.

C) diversifiable risk.

D) total risk.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following statements is false?

A) Adding additional securities to a portfolio only reduces market risk.

B) The risk-return relationship relates only to market risk.

C) Reducing market risk usually implies sacrificing expected return.

D) The appropriate measure of risk should only consider the incremental risk a security adds to a well-diversified portfolio.

E) Investors are usually not fully compensated for bearing the total risk associated with a security.

A) Adding additional securities to a portfolio only reduces market risk.

B) The risk-return relationship relates only to market risk.

C) Reducing market risk usually implies sacrificing expected return.

D) The appropriate measure of risk should only consider the incremental risk a security adds to a well-diversified portfolio.

E) Investors are usually not fully compensated for bearing the total risk associated with a security.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is a characteristic of unsystematic risk?

A) Affects one or a few firms

B) Includes events like oil price shocks

C) Cannot be reduced though diversification

D) Is the only risk that investors in the market portfolio worry about

A) Affects one or a few firms

B) Includes events like oil price shocks

C) Cannot be reduced though diversification

D) Is the only risk that investors in the market portfolio worry about

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

27

Consider a value-weighted market index that includes the two companies shown in the table.You form a portfolio to mimic the index on Day 1.The mimic portfolio is designed to earn the same return as the index.What is the portfolio weight for Company 1?

A) 15%

B) 16%

C) 17%

D) 18%

E) 19%

A) 15%

B) 16%

C) 17%

D) 18%

E) 19%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following is not a source of unsystematic risk?

A) A major economic downturn

B) A crippling labor strike

C) A competitor's successful advertising campaign

D) The departure of a firm's chief executive officer

E) The expiration of a patent

A) A major economic downturn

B) A crippling labor strike

C) A competitor's successful advertising campaign

D) The departure of a firm's chief executive officer

E) The expiration of a patent

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

29

In a well-diversified portfolio,the most relevant type of risk to a well-diversified investor is

A) interest rate risk.

B) unsystematic risk.

C) market risk.

D) exchange rate risk.

E) firm-specific risk.

A) interest rate risk.

B) unsystematic risk.

C) market risk.

D) exchange rate risk.

E) firm-specific risk.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

30

Consider a value-weighted market index that includes the two companies shown in the table.What is the percentage change in the index from Day 1 to Day 2?

A) 4.00%

B) 4.25%

C) 4.50%

D) 4.75%

E) 5.00%

A) 4.00%

B) 4.25%

C) 4.50%

D) 4.75%

E) 5.00%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

31

CISCO System's stock has a correlation with the market of 0.65.CISCO's standard deviation of returns is 45% and standard deviation of the market is 20%.What is CISCO System's beta?

A) 0.29

B) 0.85

C) 1.19

D) 1.46

E) 1.76

A) 0.29

B) 0.85

C) 1.19

D) 1.46

E) 1.76

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following statements is false?

A) Adding more unrelated securities to a portfolio reduces unsystematic risk.

B) Changes in Federal Reserve policy have more effect on systematic risk than unsystematic risk.

C) Systematic risk will increase during a recession.

D) Market risk may be reduced through diversification.

E) Oil shocks affect market risk.

A) Adding more unrelated securities to a portfolio reduces unsystematic risk.

B) Changes in Federal Reserve policy have more effect on systematic risk than unsystematic risk.

C) Systematic risk will increase during a recession.

D) Market risk may be reduced through diversification.

E) Oil shocks affect market risk.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

33

If the stock market becomes more risky (e.g.there is greater uncertainty about the economy),the beta of the market portfolio increases.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

34

A popular value-weighted index is constructed out of shares in the two companies,shown in the table below.On Day 1 you construct a portfolio that mimics the index with 15% invested in Company 1 and 85% invested in Company 2.On Day 2,what trades do you need to make in order to adjust your portfolio weights so that your portfolio earns the same return as the index from Day 2 to Day 3?

A) Buy more of Company 1 and buy more of Company 2

B) Buy more of Company 1 and sell some of Company 2

C) Sell some of Company 1 and sell some of Company 2

D) Sell some of Company 1 and buy more of Company 2

E) Make no trades

A) Buy more of Company 1 and buy more of Company 2

B) Buy more of Company 1 and sell some of Company 2

C) Sell some of Company 1 and sell some of Company 2

D) Sell some of Company 1 and buy more of Company 2

E) Make no trades

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

35

________ risk can be eliminated by diversification.

A) Market

B) Unsystematic

C) Nondiversifiable

D) Systematic

A) Market

B) Unsystematic

C) Nondiversifiable

D) Systematic

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

36

Beta is a more relevant measure of risk to an investor with a well-diversified portfolio than to an investor who holds only one stock.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

37

A popular value-weighted index is constructed out of shares in the two companies shown in the table,below.On Day 1 you construct a portfolio that mimics the index.In order for your portfolio to earn the same return as the index from Day 2 to Day 3,what portfolio weight do you need for Company 1 on Day 2?

A) 12%

B) 13%

C) 14%

D) 15%

E) 16%

A) 12%

B) 13%

C) 14%

D) 15%

E) 16%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

38

The slope of the characteristic line is beta.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

39

Consider a value-weighted market index that includes the following two companies.On Day 1 you form a portfolio to mimic the index.(In other words,to earn the same return as the index.)

What is the portfolio weight on Company 1,and what is the return on the portfolio from Day 1 to Day 2? (Weight %,Return %)

A) 14%, 5%

B) 14%, 6%

C) 15%, 6%

D) 15%, 7%

E) 16%, 5%

What is the portfolio weight on Company 1,and what is the return on the portfolio from Day 1 to Day 2? (Weight %,Return %)

A) 14%, 5%

B) 14%, 6%

C) 15%, 6%

D) 15%, 7%

E) 16%, 5%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

40

________ risk cannot be eliminated by diversification.

A) Market

B) Unsystematic

C) Firm-specific

D) Systemic

A) Market

B) Unsystematic

C) Firm-specific

D) Systemic

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

41

You manage a portfolio in which you invest half of your money in T-Bills and the other half in a mutual fund that is indexed to match the market portfolio.What is the beta of this portfolio?

A) 0

B) 0.25

C) 0.50

D) 0.75

E) 1.00

A) 0

B) 0.25

C) 0.50

D) 0.75

E) 1.00

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

42

A friend tells you about a fund that does just as well as the market in bull markets but cushions your fall in bear markets.That is,its returns fall by less than the market's in bear markets.Your friend is telling you that the fund's Beta is ________ in bull markets,but that the fund's Beta is ________ in bear markets.

A) less than one; less than one

B) less than one; equal to one

C) equal to one; less than one

D) equal to one; greater than one

E) greater than one; less than one

A) less than one; less than one

B) less than one; equal to one

C) equal to one; less than one

D) equal to one; greater than one

E) greater than one; less than one

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

43

________ shows that investors who hold the market portfolio do not care about unsystematic risk.

A) Beta

B) Capital Asset Pricing Model

C) Variance

D) Stock Market Index

A) Beta

B) Capital Asset Pricing Model

C) Variance

D) Stock Market Index

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

44

You own two mutual funds.Fund A has an expected return of 12% and a beta of 0.8.Fund B has an expected return of 18% and a beta of 1.4.If your portfolio beta is the same as the market portfolio,what proportion of your portfolio is invested in fund A?

A) 1/4

B) 1/3

C) 1/2

D) 2/3

E) 3/4

A) 1/4

B) 1/3

C) 1/2

D) 2/3

E) 3/4

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

45

Fishing supply company,Outside Tackle,has its returns graphed against the market returns for a 5 year period.The line that has the best fit for the data has the formula y = .1254 + 1.265x.What information can we derive from this?

A) The beta of Outside Tackle is .1254.

B) The systematic risk of Outside Tackle is less than average for the market.

C) The beta for Outside Tackle is 1.265.

D) Outside Tackle has posted better returns than the market for this time period.

A) The beta of Outside Tackle is .1254.

B) The systematic risk of Outside Tackle is less than average for the market.

C) The beta for Outside Tackle is 1.265.

D) Outside Tackle has posted better returns than the market for this time period.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

46

Your portfolio had a beta of 1.233.The portfolio included two stocks.The first stock had a beta of 0.7 and the second had a beta of 1.1.What were the portfolio weights for each stock?

A) -0.333 in stock 1; 1.333 in stock 2

B) -0.333 in stock 2; 1.333 in stock 1

C) 0.333 in stock 1; 0.667 in stock 2

D) 0.333 in stock 2; 0.667 in stock 1

E) None of the above.

A) -0.333 in stock 1; 1.333 in stock 2

B) -0.333 in stock 2; 1.333 in stock 1

C) 0.333 in stock 1; 0.667 in stock 2

D) 0.333 in stock 2; 0.667 in stock 1

E) None of the above.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

47

Your friend tells you that the Prudent Mutual Fund gives you more downside protection than buying an exchange traded fund (ETF)that mimics the market portfolio.What is he telling you about the fund's Beta?

A) β < 1

B) β > 1

C) β = 1

D) β = 0

A) β < 1

B) β > 1

C) β = 1

D) β = 0

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

48

Last year the market's return was 7% and Hare Growth earned 9%.This year the market was up and yielded 17%.If Hare Growth's Beta is 1.75,then what is Hare's return this year?

A) 12.25%

B) 15.75%

C) 17.50%

D) 24.50%

E) 26.50%

A) 12.25%

B) 15.75%

C) 17.50%

D) 24.50%

E) 26.50%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

49

You hold the following portfolio,consisting of Assets A,B and C.What is the portfolio beta?

A) 0.75

B) 1.00

C) 1.05

D) 1.15

E) 1.25

A) 0.75

B) 1.00

C) 1.05

D) 1.15

E) 1.25

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

50

The table below gives the historic return over the past five months for the market portfolio and two assets: A and B.Which of the answers below best describes the historic beta for A and B?

A) βA < 0; βB = 0

B) βA > 0; βB = +1

C) βA > 0; βB = 0

D) βA > +1; βB = 0

E) βA < -1; βB = +1

A) βA < 0; βB = 0

B) βA > 0; βB = +1

C) βA > 0; βB = 0

D) βA > +1; βB = 0

E) βA < -1; βB = +1

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

51

A friend tells you about a mutual fund that can protect you on the downside.In other words,in bear markets the return on the mutual fund does not fall as much as the market's return.The fund's Beta is:

A) Greater than one

B) Equal to one

C) Less than one

A) Greater than one

B) Equal to one

C) Less than one

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

52

You manage your own portfolio of about twenty stocks.One of which is Honda Motors.The returns on Honda tend to move up and down with the economy as a whole.You decide to sell Honda and replace it with the common stock of Repo-Man Inc.,an asset recovery company.Repo-Man's shares tend to rise when the economy falls,and vice versa.Your portfolio's beta should:

A) Decrease

B) Increase

C) Remain unchanged

D) Either Increase or Decrease

A) Decrease

B) Increase

C) Remain unchanged

D) Either Increase or Decrease

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

53

What is the Beta for a security whose returns do not vary across states of nature (a risk-free security)?

A) 0

B) Between 0 and 1

C) 1

D) > 1

E) < 0

A) 0

B) Between 0 and 1

C) 1

D) > 1

E) < 0

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

54

The change of risk in a portfolio from the addition of one more share of a particular asset to the portfolio is called

A) CAPM.

B) marginal risk.

C) market risk.

D) diversifiable risk.

A) CAPM.

B) marginal risk.

C) market risk.

D) diversifiable risk.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following statements concerning beta is correct?

A) Its calculation is unnecessary and too complicated to be used efficiently.

B) The risk free asset is equal to 1.

C) The portfolio beta is the sum of the single asset betas.

D) It measures the amount of systematic risk possessed by an individual asset.

A) Its calculation is unnecessary and too complicated to be used efficiently.

B) The risk free asset is equal to 1.

C) The portfolio beta is the sum of the single asset betas.

D) It measures the amount of systematic risk possessed by an individual asset.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

56

You own a stock portfolio invested 30% in a film company,20% in a bank stock,10% in a mining company,and 40% in an oil company.The betas of these four stocks are 1.4,0.6,1.5,and 1.8 respectively.What is the portfolio beta?

A) 1.00

B) 1.20

C) 1.35

D) 1.41

E) 1.50

A) 1.00

B) 1.20

C) 1.35

D) 1.41

E) 1.50

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

57

In the Capital Asset Pricing Model (CAPM),beta measures

A) the standard deviation of a single asset.

B) the price volatility of a single security not held in a portfolio.

C) the degree of correlation between two securities.

D) the historical relationship between the returns from an asset and the returns from the efficient portfolio.

E) the firm-specific risk of an asset.

A) the standard deviation of a single asset.

B) the price volatility of a single security not held in a portfolio.

C) the degree of correlation between two securities.

D) the historical relationship between the returns from an asset and the returns from the efficient portfolio.

E) the firm-specific risk of an asset.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

58

Refer to the data in the table.Which asset possesses the greatest amount of systematic risk?

A) A

B) B

C) C

D) Both A and C

E) Impossible to tell, given the above information

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

59

The points that do not fall onto the characteristic line for a company don't do so because of

A) Market risk.

B) Non-Diversifiable risk.

C) Total Risk.

D) Firm-Specific risk.

E) Standard Deviation of Returns.

A) Market risk.

B) Non-Diversifiable risk.

C) Total Risk.

D) Firm-Specific risk.

E) Standard Deviation of Returns.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

60

The table below gives the historic return over the past five months for the market portfolio and two assets: A and B.Which of the answers below best describes the historic beta for A and B?

A) βA < 1; βB < 1

B) βA = 0; βB < 1

C) βA = 0; βB > 0

D) βA > 1; βB > 1

E) βA < 1; βB > 1

A) βA < 1; βB < 1

B) βA = 0; βB < 1

C) βA = 0; βB > 0

D) βA > 1; βB > 1

E) βA < 1; βB > 1

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

61

The beta of a portfolio

A) does not change over time.

B) is irrelevant, only the betas of the individual assets are important.

C) is the weighted average of the betas of the individual assets in the portfolio.

D) is the sum of the betas of all assets in the portfolio.

A) does not change over time.

B) is irrelevant, only the betas of the individual assets are important.

C) is the weighted average of the betas of the individual assets in the portfolio.

D) is the sum of the betas of all assets in the portfolio.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

62

You want to buy $20,000 worth of shares in Tootsie Roll Industries Inc.on margin,but you only have $10,000 of your own money to invest.The remaining $10,000 is borrowed by issuing T-Bills; assume the cost of borrowing is the risk-free rate.The weight of Tootsie Roll Industries in your portfolio is 2.0.The weight of T-Bills in your portfolio is -1.0.Assume that Tootsie Roll has a beta of 0.75.What is the beta of the portfolio?

A) 0.75

B) 1.25

C) 1.50

D) 1.75

E) 2.00

A) 0.75

B) 1.25

C) 1.50

D) 1.75

E) 2.00

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

63

You want to buy $20,000 worth of shares in Tootsie Roll Industries Inc.on margin,but you only have $10,000 of your own money to invest.The remaining $10,000 is borrowed by issuing T-Bills; assume the cost of borrowing is the risk-free rate.What is the portfolio weight for Tootsie Roll?

A) 0.25

B) 0.50

C) 1.00

D) 1.50

E) 2.00

A) 0.25

B) 0.50

C) 1.00

D) 1.50

E) 2.00

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

64

Consider the two assets outlined in the table below.What is the beta of the two asset portfolio given that 40% is invested in X?

A) 0.026

B) 0.085

C) 0.160

D) 0.190

E) 0.220

A) 0.026

B) 0.085

C) 0.160

D) 0.190

E) 0.220

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

65

Peter Lynch has the following portfolio of investments:

What is the beta of Peter's portfolio?

A) 1.000

B) 1.126

C) 1.366

D) 1.534

E) 1.877

What is the beta of Peter's portfolio?

A) 1.000

B) 1.126

C) 1.366

D) 1.534

E) 1.877

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

66

You want to buy $20,000 worth of shares in Tootsie Roll Industries Inc.on margin,but you only have $10,000 of your own money to invest.The remaining $10,000 is borrowed by issuing T-Bills; assume the cost of borrowing is the risk-free rate.The weight of Tootsie Roll Industries in your portfolio is 2.0.The weight of T-Bills in your portfolio is -1.0.Assume that the expected return on Tootsie Roll is 12% and the expected return on the risk free asset (T-Bills)is 5%.What is the return on your portfolio?

A) 17%

B) 18%

C) 19%

D) 20%

E) 21%

A) 17%

B) 18%

C) 19%

D) 20%

E) 21%

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

67

Your video-game addicted nephew tells you that the Nintendo Wii is much better than the Microsoft X-Box.To take advantage of this information,you decide to build a two asset portfolio by buying shares in Nintendo and selling shares short in Microsoft.For your long position you buy 1700 shares of Nintendo at a price of $40 per share.For the short position,you sell 1000 shares in Microsoft at a price of $35 per share.What is the portfolio weight for your short position in Microsoft?

A) -1.06

B) -0.94

C) 0

D) 0.34

E) 0.50

A) -1.06

B) -0.94

C) 0

D) 0.34

E) 0.50

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

68

You are looking over your brother's portfolio.In his portfolio,he is holding one long position and one short position.Jimmy,your brother,bought 1,600 shares of Sunny Inc.each for $55.He sold 1,000 shares of Rainy Ltd.for $50 a share.Calculate the portfolio weight on the Rainy Ltd.position.

A) -1.32

B) -0.76

C) -0.50

D) 0.24

E) 0.30

A) -1.32

B) -0.76

C) -0.50

D) 0.24

E) 0.30

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

69

A beta coefficient of + 1 represents an asset that

A) is unaffected by market movement.

B) is less responsive than the market portfolio.

C) has the same response as the market portfolio.

D) is more responsive than the market portfolio.

A) is unaffected by market movement.

B) is less responsive than the market portfolio.

C) has the same response as the market portfolio.

D) is more responsive than the market portfolio.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

70

A friend tips you off on a hot stock: Sure Thing Mines Ltd.You only have $10,000 to invest but you want to invest more.Assume that you can borrow an additional $5,000 by short-selling the risk free asset (issuing T-Bills).You purchase $15,000 worth of shares in Sure Thing Mines Ltd.

The expected returns and standard deviations of the two assets are outlined in the table below:

What is the beta of the portfolio?

A) 1.50

B) 1.70

C) 2.50

D) 2.55

E) 2.70

The expected returns and standard deviations of the two assets are outlined in the table below:

What is the beta of the portfolio?

A) 1.50

B) 1.70

C) 2.50

D) 2.55

E) 2.70

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

71

You own a portfolio that is equally invested in three assets: 1)the risk-free asset; 2)Stock 1; and 3)Stock 2.Stock 1 has a beta of 1.9 and the portfolio has the same risk as the market portfolio.

What is the beta of Stock 2 in the portfolio?

A) 1.0

B) 1.1

C) 1.2

D) 1.3

E) 1.4

What is the beta of Stock 2 in the portfolio?

A) 1.0

B) 1.1

C) 1.2

D) 1.3

E) 1.4

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

72

An individual's portfolio consists of three separate assets.Asset 1 has a beta of 1.4,asset 2 has a beta of .84 and asset 3 has a beta of 1.05.The investor has invested $240 in asset 1,$500 in asset 2,and $260 in asset 3.Calculate the portfolio beta.

A) 1.03

B) 1.17

C) 1.09

D) 0.93

E) 0.85

A) 1.03

B) 1.17

C) 1.09

D) 0.93

E) 0.85

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

73

The beta of the market

A) is 1.

B) is greater than 1.

C) cannot be determined.

D) is less than 1.

A) is 1.

B) is greater than 1.

C) cannot be determined.

D) is less than 1.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

74

A friend brags that she expects to earn a return of 10.25% on her portfolio with a beta of 0.825.Can you match her performance with Stock X (12% return and a beta of 1.1)and the risk free asset that earns a 5% return? With what portfolio weights?

A) Yes, 0.75 Stock X and 0.25 Risk Free Asset

B) Yes, 0.25 Stock X and 0.75 Risk Free Asset

C) Yes, 0.5 Stock X and 0.5 Risk Free Asset

D) No

A) Yes, 0.75 Stock X and 0.25 Risk Free Asset

B) Yes, 0.25 Stock X and 0.75 Risk Free Asset

C) Yes, 0.5 Stock X and 0.5 Risk Free Asset

D) No

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

75

Beta is the slope of the security market line.

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

76

You want to buy $20,000 worth of shares in Tootsie Roll Industries Inc.on margin,but you only have $10,000 of your own money to invest.The remaining $10,000 is borrowed by issuing T-Bills; assume the cost of borrowing is the risk-free rate.What is the portfolio weight for the risk free asset (T-Bills)?

A) -1.00

B) -0.50

C) 1.00

D) 0.50

E) 2.00

A) -1.00

B) -0.50

C) 1.00

D) 0.50

E) 2.00

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

77

Your friend,Dobson,manages the Formula Growth mutual fund.Dobson expects to earn 11% on his portfolio with a beta of 1.2.You only invest in shares of General Electric and T-Bills.You like GE because it was started in 1890 by Thomas Edison,the great American inventor,and it has a diversified portfolio of products including jet engines and MRI diagnostic imaging machines.The expected return of GE is 13% and its beta is 1.40.The expected return on T-Bills is 2%.If you construct your portfolio so that its risk is equal to the risk of Formula Growth,then what portfolio weight do you need on the shares of GE?

A) 0.85

B) 0.86

C) 0.87

D) 0.88

E) 0.89

A) 0.85

B) 0.86

C) 0.87

D) 0.88

E) 0.89

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

78

Warren has a portfolio with three stocks as shown in the table.What is the beta of Warren's portfolio?

A) 0.775

B) 0.988

C) 1.017

D) 1.340

E) 1.505

A) 0.775

B) 0.988

C) 1.017

D) 1.340

E) 1.505

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

79

If Acme Dynamite stock has a beta of .8 and a standard deviation of 15% and Splat Paintball stock has a beta of 1.3 and a standard deviation of 9%,what is the beta of a portfolio comprised of equal weights of both securities?

A) 24%

B) 12%

C) 18%

D) 1.05

E) 2.10

A) 24%

B) 12%

C) 18%

D) 1.05

E) 2.10

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

80

Tom wishes to calculate the riskiness of his portfolio,which is comprised of equal amounts of two stocks.Which of the following measures would you recommend?

A) Weighted average betas of the two securities

B) A weighted average of the correlation between the two securities

C) Weighted average standard deviations

D) The slope of the security market line

E) A weighted average of the coefficients of variation

A) Weighted average betas of the two securities

B) A weighted average of the correlation between the two securities

C) Weighted average standard deviations

D) The slope of the security market line

E) A weighted average of the coefficients of variation

Unlock Deck

Unlock for access to all 136 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 136 flashcards in this deck.