Deck 19: Corporations: Distributions Not in Complete Liquidation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Scarlet Corporation (a calendar year taxpayer)has taxable income of $150,000,and its financial records reflect the following for the year.  Scarlet Corporation's current E & P is:

Scarlet Corporation's current E & P is:

A) $127,000.

B) $107,000.

C) $97,000.

D) $57,000.

E) None of the above.

Scarlet Corporation's current E & P is:A) $127,000.

B) $107,000.

C) $97,000.

D) $57,000.

E) None of the above.

Question

Question

Platinum Corporation,a calendar year taxpayer,has taxable income of $500,000.Among its transactions for the year are the following:  Disregarding any provision for Federal income taxes,Platinum Corporation's current E & P is:

Disregarding any provision for Federal income taxes,Platinum Corporation's current E & P is:

A) $455,000.

B) $535,000.

C) $545,000.

D) $625,000.

E) None of the above.

Disregarding any provision for Federal income taxes,Platinum Corporation's current E & P is:A) $455,000.

B) $535,000.

C) $545,000.

D) $625,000.

E) None of the above.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

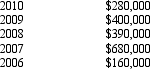

Duck Corporation is a calendar year taxpayer formed in 2005.Duck's E & P for each of the past 5 years is listed below.  Duck Corporation made the following distributions in the previous 5 years.

Duck Corporation made the following distributions in the previous 5 years.

2009 Land (basis of $700,000,fair market value of $800,000)

2006 $200,000 cash

Duck's accumulated E & P as of January 1,2011 is:

A) $910,000.

B) $950,000.

C) $1,010,000.

D) $1,050,000.

E) None of the above.

Duck Corporation made the following distributions in the previous 5 years.2009 Land (basis of $700,000,fair market value of $800,000)

2006 $200,000 cash

Duck's accumulated E & P as of January 1,2011 is:

A) $910,000.

B) $950,000.

C) $1,010,000.

D) $1,050,000.

E) None of the above.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/137

Play

Full screen (f)

Deck 19: Corporations: Distributions Not in Complete Liquidation

1

When computing E & P,taxable income is not adjusted for additional first-year depreciation.

False

2

A distribution in excess of E & P is treated as capital gain by shareholders.

False

3

Use of MACRS cost recovery when computing taxable income does not require an E & P adjustment.

False

4

Distributions by a corporation to its shareholders are presumed to be a return of capital unless the parties can prove otherwise.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

5

Distributions that are not dividends are a return of capital and decrease the shareholder's basis.Once basis is reduced to zero,any excess is taxed as a capital gain.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

6

An increase in the LIFO recapture amount must be added to taxable income to determine E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

7

Cash distributions received from a corporation with a positive balance in accumulated E & P at the beginning of the year will be taxed as dividend income.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

8

A realized gain from an involuntary conversion under § 1033 that is not recognized for income tax purposes has no effect on E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

9

The dividends received deduction is added back to taxable income to determine E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

10

A corporation borrows money to purchase State of Texas bonds.The interest on the loan has no impact on either taxable income or current E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

11

When computing current E & P,taxable income is not adjusted for the deferred gain in a § 1031 like-kind exchange.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

12

Federal income tax paid in the current year must be subtracted from taxable income to determine E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

13

A distribution from a corporation will be taxable to the recipient shareholders only to the extent of the corporation's E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

14

When a corporation makes an installment sale,for E & P purposes the realized gain is recognized in the year of sale.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

15

To determine E & P,some (but not all)previously excluded income items are added back to taxable income.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

16

Nondeductible meal and entertainment expenses must be subtracted from taxable income to determine current E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

17

When computing E & P,an adjustment to taxable income is necessary for any domestic production activities deduction.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

18

The terms "earnings and profits" and "retained earnings" are identical in meaning.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

19

In the current year,Pink Corporation has a § 179 expense of $80,000.As a result,next year,taxable income must be decreased by $16,000 to determine current E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

20

Any loss in current E & P must be treated as occurring ratably during the year.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

21

When current E & P has a deficit and accumulated E & P is positive,the two accounts are netted at the date of the distribution.If a positive balance results,the distribution is a dividend to the extent of the balance.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

22

During the year,Blue Corporation distributes land to its sole shareholder.If the fair market value of the land is less than its adjusted basis,Blue will recognize a loss on the distribution.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

23

If a distribution of stock rights is taxable and their fair market value is less than 15 percent of the value of the old stock,then either a zero basis or a portion of the old stock basis may be assigned to the rights,at the shareholder's option.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

24

Regardless of any deficit in current E & P,distributions during the year are taxed as dividends to the extent of accumulated E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

25

If a stock dividend is taxable,the shareholder's basis in the newly received shares is equal to the fair market value of the shares received in the distribution.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

26

A corporation that distributes a property dividend must reduce its E & P by the adjusted basis of the property less any liability on the property.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

27

Corporate distributions are presumed to be paid out of E & P and are treated as dividends unless the parties to the transaction can show otherwise.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

28

In certain circumstances,the amount of dividend income recognized by a shareholder from a property distribution is not reduced by the amount of liability assumed by a shareholder.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

29

Constructive dividends have no effect on a distributing corporation's E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

30

For tax purposes,all stock redemptions are treated as dividend distributions.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

31

Certain dividends from foreign corporations can be qualified dividends for purposes of the 15% rate available to individuals.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

32

When current E & P is positive and accumulated E & P has a deficit balance,the two accounts are netted for dividend determination purposes.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

33

Dividends paid to shareholders who hold both long and short positions do not qualify for the reduced tax rate available to individuals in certain years.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

34

Property distributed by a corporation as a dividend is subject to a liability in excess of its basis.For purposes of determining gain on the distribution,the basis of the property is treated as being not less than the amount of liability.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

35

The rules used to determine the taxability of stock dividends also apply to distributions of stock rights.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

36

A corporate shareholder that receives a constructive dividend cannot apply a dividends received deduction to the distribution.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

37

Dividends taxed as ordinary income are considered investment income for purposes of the investment interest expense limitation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

38

Constructive dividends do not need to satisfy the legal requirements for a dividend as set forth by applicable state law.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

39

Under certain circumstances,a distribution can generate (or add to)a deficit in E & P.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

40

If stock rights are taxable,the recipient has income to the extent of the fair market value of the rights.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

41

Scarlet Corporation (a calendar year taxpayer)has taxable income of $150,000,and its financial records reflect the following for the year. Scarlet Corporation's current E & P is:

A) $127,000.

B) $107,000.

C) $97,000.

D) $57,000.

E) None of the above.

Scarlet Corporation's current E & P is:A) $127,000.

B) $107,000.

C) $97,000.

D) $57,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

42

Sally and her mother are the sole shareholders of Owl Corporation.During the current year,Owl distributes cash in redemption of all of Sally's stock.Sally continues to be employed as controller for Owl after the redemption.The distribution is a complete termination redemption resulting in sale or exchange treatment for Sally.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

43

Platinum Corporation,a calendar year taxpayer,has taxable income of $500,000.Among its transactions for the year are the following: Disregarding any provision for Federal income taxes,Platinum Corporation's current E & P is:

A) $455,000.

B) $535,000.

C) $545,000.

D) $625,000.

E) None of the above.

Disregarding any provision for Federal income taxes,Platinum Corporation's current E & P is:A) $455,000.

B) $535,000.

C) $545,000.

D) $625,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

44

A shareholder's holding period of property acquired in a stock redemption begins on the date of the distribution.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

45

For a stock redemption to qualify for sale or exchange treatment under § 303 (redemption to pay death taxes),it need not satisfy any of the § 302 redemption provisions.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

46

Grackle Corporation (E & P of $600,000)distributes cash of $200,000 and land (fair market value of $400,000; basis of $250,000)to a shareholder in a qualifying stock redemption.The land distributed is subject to a mortgage of $460,000.Grackle will recognize a gain of $150,000 as a result of the distribution.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

47

As a result of a redemption,a shareholder's interest (direct and indirect)in the corporation decreased from 58% to 45%.The redemption qualifies for sale or exchange treatment as a disproportionate redemption.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

48

In a redemption to pay death taxes,stock in corporations in which the decedent held a 20% or more interest is treated as stock in a single corporation for purposes of determining whether the value of stock owned by the decedent exceeds 35% of the value of the decedent's adjusted gross estate.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

49

Vireo Corporation redeemed shares from its sole shareholder pursuant to a written agreement between the parties that clearly identified the transaction as a stock redemption (and not a dividend distribution).Since the agreement is binding under state law,the shareholder will receive sale or exchange treatment with respect to the redemption.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

50

The tax treatment of corporate distributions at the shareholder level does not depend on:

A) The character of the property being distributed.

B) The earnings and profits of the corporation.

C) The basis of stock in the hands of the shareholder.

D) Whether the distributed property is received by an individual or a corporation.

E) None of the above.

A) The character of the property being distributed.

B) The earnings and profits of the corporation.

C) The basis of stock in the hands of the shareholder.

D) Whether the distributed property is received by an individual or a corporation.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

51

Puffin Corporation's 2,000 shares outstanding are owned as follows: Paul,800 shares; Sandra (Paul's sister),800 shares; and Greta (Paul's granddaughter),400 shares.During the current year,Puffin (E & P of $1 million)redeemed 600 shares of Paul's stock for $100,000.If Paul had acquired the 600 shares five years ago for $30,000,he will have a long-term capital gain of $70,000 from the redemption.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

52

Noncorporate shareholders generally prefer a nonqualified stock redemption over a qualifying stock redemption due to the availability of the dividends received deduction.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

53

In a not essentially equivalent redemption [§ 302(b)(1)],the meaningful reduction test is an objective safe harbor rule that taxpayers can rely upon for sale or exchange treatment.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

54

In applying the stock attribution rules to a stock redemption,stock owned by a shareholder who owns 65% of a corporation is deemed to be owned in full by the corporation.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

55

In 2008,Floyd carried out a successful complete termination redemption of his stock in Gray Corporation.Floyd was able to qualify the transaction as a complete termination redemption only by use of the family attribution waiver.In 2011,Floyd receives stock in Gray Corporation as a gift from his father.Floyd has acquired a prohibited interest within the 10-year postredemption period and,as a result,the 2008 redemption no longer qualifies as a complete termination redemption.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

56

A shareholder's basis in property received in a stock redemption is the property's fair market value.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

57

Blue Corporation,a cash basis taxpayer,has taxable income of $700,000 for the current year.Blue elected $80,000 of § 179 expense.It also had a related party loss of $30,000 and a realized (not recognized)gain from an involuntary conversion of $85,000.It paid Federal income tax of $185,000 and a nondeductible fine of $20,000.Blue's current E & P is:

A) $465,000.

B) $529,000.

C) $614,000.

D) $630,000.

E) None of the above.

A) $465,000.

B) $529,000.

C) $614,000.

D) $630,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

58

Betty's adjusted gross estate is $7 million.The death taxes and funeral and administration expenses of her estate total $800,000.Included in Betty's gross estate is stock in Heron Corporation,valued at $2.1 million as of the date of her death in 2011.Betty had acquired the stock six years ago at a cost of $410,000.If Heron Corporation redeems $800,000 of Heron stock from the estate,the transaction will qualify under § 303 as a redemption to pay death taxes and receive sale or exchange treatment.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

59

At a time when Blackbird Corporation had E & P of $700,000 and 1,000 shares of stock outstanding,the corporation distributed $300,000 to redeem 400 shares of its stock.The transaction qualified as a disproportionate redemption for the shareholder.Blackbird's E & P is reduced by $280,000 as a result of the distribution.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

60

Reginald and Roland (Reginald's son)each own 50% of the stock of Robin Corporation.Reginald's stock interest is entirely redeemed by Robin Corporation.Two years later,Reginald loans Robin Corporation $250,000.The loan to Robin Corporation constitutes a prohibited interest for purposes of the family attribution waiver.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

61

Gander,a calendar year corporation,has a deficit in current E & P of $100,000 and a $290,000 positive balance in accumulated E & P.If Gander determines that a $500,000 distribution to its shareholders is appropriate at some point during the year,what is the maximum amount of the distribution that could potentially be treated as a dividend?

A) $0.

B) $190,000.

C) $240,000.

D) $290,000.

E) None of the above.

A) $0.

B) $190,000.

C) $240,000.

D) $290,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

62

Tungsten Corporation,a calendar year cash basis taxpayer,made estimated tax payments of $800 each quarter in 2011,for a total of $3,200.Tungsten filed its 2011 tax return in 2012 and the return showed a tax liability $4,200.At the time of filing,March 15,2012,Tungsten paid an additional $1,000 in Federal income taxes.How does the additional payment of $1,000 impact Tungsten's E & P?

A) Increase by $1,000 in 2011.

B) Increase by $1,000 in 2012.

C) Decrease by $1,000 in 2011.

D) Decrease by $1,000 in 2012.

E) None of the above.

A) Increase by $1,000 in 2011.

B) Increase by $1,000 in 2012.

C) Decrease by $1,000 in 2011.

D) Decrease by $1,000 in 2012.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

63

On January 1,Gull Corporation (a calendar year taxpayer)has accumulated E & P of $200,000.During the year,Gull incurs a net loss of $280,000 from operations that accrues ratably.On June 30,Gull distributes $120,000 to Sharon,its sole shareholder,who has a basis in her stock of $75,000.How much of the $120,000 is a dividend to Sharon?

A) $0.

B) $60,000.

C) $75,000.

D) $120,000.

E) None of the above.

A) $0.

B) $60,000.

C) $75,000.

D) $120,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

64

At the beginning of the current year,Doug and Alfred each own 50% of Amaryllis Corporation (a calendar year taxpayer).In July,Doug sold his stock to Kevin for $140,000.At the beginning of the year,Amaryllis Corporation had accumulated E & P of $240,000 and its current E & P is $280,000 (prior to any distributions).Amaryllis distributed $300,000 on February 15 ($150,000 to Doug and $150,000 to Alfred)and distributed another $300,000 on November 1 ($150,000 to Kevin and $150,000 to Alfred).Kevin has dividend income of:

A) $150,000.

B) $140,000.

C) $110,000.

D) $70,000.

E) None of the above.

A) $150,000.

B) $140,000.

C) $110,000.

D) $70,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

65

Duck Corporation is a calendar year taxpayer formed in 2005.Duck's E & P for each of the past 5 years is listed below. Duck Corporation made the following distributions in the previous 5 years.

2009 Land (basis of $700,000,fair market value of $800,000)

2006 $200,000 cash

Duck's accumulated E & P as of January 1,2011 is:

A) $910,000.

B) $950,000.

C) $1,010,000.

D) $1,050,000.

E) None of the above.

Duck Corporation made the following distributions in the previous 5 years.2009 Land (basis of $700,000,fair market value of $800,000)

2006 $200,000 cash

Duck's accumulated E & P as of January 1,2011 is:

A) $910,000.

B) $950,000.

C) $1,010,000.

D) $1,050,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

66

Glenda is the sole shareholder of Condor Corporation.She sold her stock to Melissa on October 31 for $150,000.Glenda's basis in Condor stock was $50,000 at the start of the year.Condor distributed land to Glenda immediately before the sale.Condor's basis in the land was $20,000 (fair market value of $25,000).On December 31,Melissa received a $75,000 cash distribution from Condor.During the year,Condor has $20,000 of current E & P and its accumulated E & P balance on January 1 is $10,000.Which of the following statements is true?

A) Glenda recognizes a $110,000 gain on the sale of her stock.

B) Glenda recognizes a $100,000 gain on the sale of her stock.

C) Melissa receives $5,000 of dividend income.

D) Glenda receives $20,000 of dividend income.

E) None of the above.

A) Glenda recognizes a $110,000 gain on the sale of her stock.

B) Glenda recognizes a $100,000 gain on the sale of her stock.

C) Melissa receives $5,000 of dividend income.

D) Glenda receives $20,000 of dividend income.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following is not an economic distortion created by the double tax on dividends?

A) An incentive to invest in noncorporate rather than corporate businesses.

B) An incentive for corporations to finance operations with debt rather than equity.

C) An incentive to invest domestically rather than internationally.

D) An incentive for corporations to retain earnings and structure distributions to avoid dividend treatment.

E) All of the above represent economic distortions created by the double tax on dividends.

A) An incentive to invest in noncorporate rather than corporate businesses.

B) An incentive for corporations to finance operations with debt rather than equity.

C) An incentive to invest domestically rather than internationally.

D) An incentive for corporations to retain earnings and structure distributions to avoid dividend treatment.

E) All of the above represent economic distortions created by the double tax on dividends.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

68

Tracy and Lance,equal shareholders in Macaw Corporation,receive $600,000 each in distributions on December 31 of the current year.Macaw's current year taxable income is $1 million and it has no accumulated E & P.Last year,Macaw sold an appreciated asset for $1,200,000 (basis of $400,000).Payment for one-half of the sale of the asset was made this year.How much of Tracy's distribution will be taxed as a dividend?

A) $0.

B) $300,000.

C) $500,000.

D) $600,000.

E) None of the above.

A) $0.

B) $300,000.

C) $500,000.

D) $600,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

69

As of January 1,Warbler Corporation has a deficit in accumulated E & P of $150,000.For the year,current E & P (accrued ratably)is $260,000 (prior to any distributions).On July 1,Warbler Corporation distributes $295,000 to its sole shareholder.The amount of the distribution that is a dividend is:

A) $10,000.

B) $110,000.

C) $260,000.

D) $295,000.

E) None of the above.

A) $10,000.

B) $110,000.

C) $260,000.

D) $295,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

70

Falcon Corporation has $200,000 of current E & P and a deficit in accumulated E & P of $90,000.If Swan pays a $300,000 distribution to its shareholders on July 1,how much dividend income do the shareholders report?

A) $0.

B) $10,000.

C) $110,000.

D) $200,000.

E) None of the above.

A) $0.

B) $10,000.

C) $110,000.

D) $200,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

71

Renee,the sole shareholder of Indigo Corporation,sold her stock to Chad on July 1 for $180,000.Renee's stock basis at the beginning of the year was $120,000.Indigo made a $60,000 cash distribution to Renee immediately before the sale,while Chad received a $120,000 cash distribution from Indigo on November 1.As of the beginning of the current year,Indigo had $26,000 in accumulated E & P,while current E & P (before distributions)was $90,000.Which of the following statements is correct?

A) Renee recognizes a $60,000 gain on the sale of the stock.

B) Renee recognizes a $64,000 gain on the sale of the stock.

C) Chad recognizes dividend income of $120,000.

D) Chad recognizes dividend income of $30,000.

E) None of the above.

A) Renee recognizes a $60,000 gain on the sale of the stock.

B) Renee recognizes a $64,000 gain on the sale of the stock.

C) Chad recognizes dividend income of $120,000.

D) Chad recognizes dividend income of $30,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

72

Ashley and Andrew,equal shareholders in Parrot Corporation,receive $250,000 each in distributions on December 31 of the current year.During the current year,Parrot sold an appreciated asset for $500,000 (basis of $150,000).Payment for the sale of the asset will be made as follows: 50% next year and 50% in the following year,with interest payable at a rate of 7.5%.Before considering the effect of the asset sale,Parrot's current year E & P is $400,000 and it has no accumulated E & P.How much of Ashley's distribution will be taxed as a dividend?

A) $0.

B) $200,000.

C) $250,000.

D) $425,000.

E) None of the above.

A) $0.

B) $200,000.

C) $250,000.

D) $425,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

73

Tangelo Corporation has an August 31 year-end.Tangelo had $50,000 in accumulated E & P at the beginning of its 2012 fiscal year (September 1,2011)and during the year,it incurred a $75,000 operating loss.It also distributed $65,000 to its sole shareholder,Cass,on November 30,2011.If Cass is a calendar year taxpayer,how should she treat the distribution when she files her 2011 income tax return (assuming the return is filed by April 15,2012)?

A) $65,000 of dividend income.

B) $60,000 of dividend income and $5,000 recovery of capital.

C) $50,000 of dividend income and $15,000 recovery of capital.

D) The distribution has no effect on Cass in the current year.

E) None of the above.

A) $65,000 of dividend income.

B) $60,000 of dividend income and $5,000 recovery of capital.

C) $50,000 of dividend income and $15,000 recovery of capital.

D) The distribution has no effect on Cass in the current year.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

74

Orange Corporation has a deficit in accumulated E & P of $600,000 and has current E & P of $450,000.On July 1,Orange distributes $500,000 to its sole shareholder,Morris,who has a basis in his stock of $105,000.As a result of the distribution,Morris has:

A) Dividend income of $450,000 and reduces his stock basis to $55,000.

B) Dividend income of $105,000 and reduces his stock basis to zero.

C) Dividend income of $450,000 and no adjustment to stock basis.

D) No dividend income, reduces his stock basis to zero, and has a capital gain of $500,000.

E) None of the above.

A) Dividend income of $450,000 and reduces his stock basis to $55,000.

B) Dividend income of $105,000 and reduces his stock basis to zero.

C) Dividend income of $450,000 and no adjustment to stock basis.

D) No dividend income, reduces his stock basis to zero, and has a capital gain of $500,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

75

On January 2,2011,Orange Corporation purchased equipment for $300,000 with an ADS recovery period of 10 years and a MACRS useful life of 7 years.Section 179 was not elected.MACRS depreciation properly claimed on the asset,including depreciation in the year of sale,totaled $79,605.The equipment was sold on July 1,2012,for $290,000.As a result of the sale,the adjustment to taxable income needed to arrive at current E & P is:

A) No adjustment is required.

B) Decrease $49,605.

C) Increase $49,605.

D) Decrease $79,605.

E) None of the above.

A) No adjustment is required.

B) Decrease $49,605.

C) Increase $49,605.

D) Decrease $79,605.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

76

Maria and Christopher each own 50% of Cockatoo Corporation,a calendar year taxpayer.Distributions from Cockatoo are: $750,000 to Maria on April 1 and $250,000 to Christopher on May 1.Cockatoo's current E & P is $300,000 and its accumulated E & P is $600,000.How much of the accumulated E & P is allocated to Christopher's distribution?

A) $0.

B) $75,000.

C) $150,000.

D) $300,000.

E) None of the above.

A) $0.

B) $75,000.

C) $150,000.

D) $300,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

77

Pheasant Corporation ended its first year of operations with taxable income of $225,000.At the time of Pheasant's formation,it incurred $50,000 of organizational expenses.In calculating its taxable income for the year,Pheasant claimed an $8,000 deduction for the organizational expenses.What is Pheasant's current E & P?

A) $175,000.

B) $183,000.

C) $225,000.

D) $233,000.

E) None of the above.

A) $175,000.

B) $183,000.

C) $225,000.

D) $233,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following statements is incorrect with respect to determining current E & P?

A) All tax-exempt income should be added back to taxable income.

B) Dividends received deductions should be added back to taxable income.

C) Charitable contributions in excess of the 10% of taxable income limit should be subtracted from taxable income.

D) Federal income tax refunds should be added back to taxable income.

E) None of the above statements are incorrect.

A) All tax-exempt income should be added back to taxable income.

B) Dividends received deductions should be added back to taxable income.

C) Charitable contributions in excess of the 10% of taxable income limit should be subtracted from taxable income.

D) Federal income tax refunds should be added back to taxable income.

E) None of the above statements are incorrect.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

79

Stacey and Andrew each own one-half of the stock in Parakeet Corporation,a calendar year taxpayer.Cash distributions from Parakeet are: $350,000 to Stacey on April 1 and $150,000 to Andrew on May 1.If Parakeet's current E & P is $60,000,how much is allocated to Andrew's distribution?

A) $5,000.

B) $10,000.

C) $18,000.

D) $30,000.

E) None of the above.

A) $5,000.

B) $10,000.

C) $18,000.

D) $30,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

80

During the current year,Goose Corporation sold equipment for $500,000 (adjusted basis of $260,000).The equipment was purchased a few years ago for $560,000 and $300,000 in MACRS deductions have been claimed.ADS depreciation would have been $200,000.As a result of the sale,the adjustment to taxable income needed to determine current E & P is:

A) No adjustment is required.

B) Subtract $100,000.

C) Add $100,000.

D) Add $80,000.

E) None of the above.

A) No adjustment is required.

B) Subtract $100,000.

C) Add $100,000.

D) Add $80,000.

E) None of the above.

Unlock Deck

Unlock for access to all 137 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 137 flashcards in this deck.