Deck 20: Forming and Operating Partnerships

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

J&J, LLC was in its third year of operations when J&J decided to expand the number of members from two, A & B, with equal profits and capital interests to three members, A, B, and

C.The third member, C, will contribute her financial expertise to the LLC in exchange for a 1/3 capital interest in J&J.Given the balance sheet below reflecting the financial position of J&J on the date member C is admitted, what are the tax consequences to members A, B, and C, and to J&J when C receives her capital interest? If, instead, member C receives a 1/3 profit interest, what would be the tax consequences to members A, B, and C, and to J&J?

C.The third member, C, will contribute her financial expertise to the LLC in exchange for a 1/3 capital interest in J&J.Given the balance sheet below reflecting the financial position of J&J on the date member C is admitted, what are the tax consequences to members A, B, and C, and to J&J when C receives her capital interest? If, instead, member C receives a 1/3 profit interest, what would be the tax consequences to members A, B, and C, and to J&J?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/100

Play

Full screen (f)

Deck 20: Forming and Operating Partnerships

1

A partnership with a C corporation partner must always use the accrual method as its accounting method.

False

2

Partnerships can use special allocations to shift built-in gains and built-in losses on contributed property from a partner who contributed the property to other partners.

False

3

A general partner's share of ordinary business income is similar to investment income; thus, a general partner only includes their guaranteed payments as self-employment income.

False

4

An additional allocation of partnership debt or relief of partnership debt is considered to be a deemed cash contribution or cash distribution respectively.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

5

The character of each separately-stated item is determined at the partner level.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

6

Tax elections are rarely made at the partnership level.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

7

Adjustments to a partner's outside basis are made annually to prevent double taxation on the sale of a partnership interest or at the time of a partnership distribution.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

8

For partnership tax years ending after December 31, 2015, partnerships can request up to a six-month extension by filing IRS Form 7004 prior to the original due date of the partnership return.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

9

A purchased partnership interest has a holding period beginning on the date of purchase regardless of the type of property held by the partnership.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

10

Partners must generally treat the value of profits interests they receive in exchange for services as ordinary income.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

11

A partnership can elect to amortize organization and startup costs; however, syndication costs are not deductible.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

12

Guaranteed payments are included in the calculation of a partnership's ordinary business income (loss) and are also treated as separately-stated items.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

13

The least aggregate deferral test uses the profit percentage of each partner to determine the minimum amount of tax deferral for the partner group as a whole in determining the permissible tax year-end of a partnership.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

14

The term "outside basis" refers to the partnership's basis in its assets; whereas, the term "inside basis" refers an individual partner's basis in her partnership interest.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

15

Partners adjust their outside basis by adding non-deductible expenses and subtracting any tax-exempt income to avoid being double taxed.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

16

Income earned by flow-through entities is usually taxed only once at the entity level.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

17

Actual or deemed cash distributions in excess of a partner's outside basis are generally taxable as capital gains.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

18

Nonrecourse debt is generally allocated according to the profit-sharing ratios of the partnership.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

19

A partner's outside basis must first be decreased by any negative basis adjustments and then increased by any positive basis adjustments.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

20

Partnerships tax rules incorporate both the entity and aggregate approaches.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following statements is true when property is contributed in exchange for a partnership interest?

A)Any contributed property in a partnership has a carryover basis, and the character of the property is determined by the way the contributing partner used the property.

B)The partnership's inside basis is typically increased by any gain the partner recognizes from the property contribution.

C)The holding period for a partner's partnership interest depends upon the type of assets a partner contributes.

D)Services are not allowed to be contributed to a partnership in return for a partnership interest.

E)All of these are true.

A)Any contributed property in a partnership has a carryover basis, and the character of the property is determined by the way the contributing partner used the property.

B)The partnership's inside basis is typically increased by any gain the partner recognizes from the property contribution.

C)The holding period for a partner's partnership interest depends upon the type of assets a partner contributes.

D)Services are not allowed to be contributed to a partnership in return for a partnership interest.

E)All of these are true.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

22

Any losses that exceed the tax basis of a partner in their partnership interest are suspended and carried forward for 20 years.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following entities is not considered a flow-through entity?

A)C corporation

B)S corporation

C)Limited Liability Company (LLC)

D)Partnership

A)C corporation

B)S corporation

C)Limited Liability Company (LLC)

D)Partnership

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following does not represent a tax election available to either partners or partnerships?

A)Electing to change an accounting method

B)Electing to amortize organization costs

C)Electing to expense a portion of syndication costs

D)Electing to immediately expense depreciable property under Section 179

A)Electing to change an accounting method

B)Electing to amortize organization costs

C)Electing to expense a portion of syndication costs

D)Electing to immediately expense depreciable property under Section 179

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

25

The main difference between a partner's tax basis and at-risk amount is that qualified nonrecourse financing is not included in the at-risk basis amount.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

26

Gerald received a one-third capital and profit (loss) interest in XYZ Limited Partnership (LP). In exchange for this interest, Gerald contributed a building with a FMV of $30,000. His adjusted basis in the building was $15,000. In addition, the building was encumbered with a $9,000 nonrecourse mortgage that XYZ, LP assumed at the time the property was contributed. What is Gerald's outside basis immediately after his contribution?

A)$6,000

B)$9,000

C)$21,000

D)$24,000

A)$6,000

B)$9,000

C)$21,000

D)$24,000

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

27

Partnerships may maintain their capital accounts according to which of the following rules?

A)GAAP

B)704(b)

C)Tax

D)Any of these

E)Only GAAP and 704(b)

A)GAAP

B)704(b)

C)Tax

D)Any of these

E)Only GAAP and 704(b)

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

28

Zinc, LP was formed on August 1, 20X9. When the partnership was formed, Al contributed $10,000 in cash and inventory with a FMV and tax basis of $40,000. In addition, Bill contributed equipment with a FMV of $30,000 and adjusted basis of $25,000 along with accounts receivable with a FMV and tax basis of $20,000. Also, Chad contributed land with a FMV of $50,000 and tax basis of $35,000. Finally, Dave contributed a machine, secured by $35,000 of debt, with a FMV of $15,000 and a tax basis of $10,000. What is the total inside basis of all the assets contributed to Zinc, LP?

A)$140,000

B)$165,000

C)$175,000

D)$200,000

A)$140,000

B)$165,000

C)$175,000

D)$200,000

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

29

Tom is talking to his friend Bob, who has an interest in Freedom, LLC, about purchasing his LLC interest. Bob's outside basis in Freedom, LLC is $10,000. This includes his $2,500 one-fourth share of the LLC's debt. Bob's 704(b) capital account is $17,000. If Tom bought Bob's LLC interest for $17,000, what would Tom's outside basis be in Freedom, LLC?

A)$10,000

B)$14,500

C)$17,000

D)$19,500

A)$10,000

B)$14,500

C)$17,000

D)$19,500

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

30

Sarah, Sue, and AS Inc. formed a partnership on May 1, 20X9 called SSAS, LP. Now that the partnership is formed, they must determine its appropriate year-end. Sarah has a 30% profits and capital interest while Sue has a 35% profits and capital interest. Both Sarah and Sue have calendar year-ends. AS Inc. holds the remaining profits and capital interest in the LP, and it has a September 30 year-end. What tax year-end must SSAS, LP use for 20X9 and which test or rule requires this year-end?

A)9/30, majority interest taxable year

B)12/31, majority interest taxable year

C)12/31, principal partners test

D)12/31, least aggregate deferral test

A)9/30, majority interest taxable year

B)12/31, majority interest taxable year

C)12/31, principal partners test

D)12/31, least aggregate deferral test

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

31

XYZ, LLC has several individual and corporate members. Abe and Joe, individuals with 4/30 year-ends, each have a 23% profits and capital interest. RST, Inc., a corporation with a 6/30 year end, owns a 4% profits and capital interest while DEF, Inc., a corporation with an 8/30 year end, owns a 4.9% profits and capital interest. Finally, thirty other calendar year-end individual partners (each with less than a 2% profits and capital interest) own the remaining 45% of the profits and capital interests in XYZ. What tax year-end should XYZ use and which test or rule requires this year-end?

A)4/30, principal partners test

B)4/30, least aggregate deferral test

C)12/31, principal partners test

D)12/31, least aggregate deferral test

A)4/30, principal partners test

B)4/30, least aggregate deferral test

C)12/31, principal partners test

D)12/31, least aggregate deferral test

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

32

If a partner participates in partnership activities on a regular, continuous, and substantial basis, then the partnership's activities with respect to this individual partner are not considered passive.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

33

In X1, Adam and Jason formed ABC, LLC, a car dealership in Kansas City. In X2, Adam and Jason realized they needed an advertising expert to assist in their business. Thus, the two members offered Cory, a marketing expert, a 1/3 capital interest in their partnership for contributing his expert services. Cory agreed to this arrangement and received his capital interest in X2. If the value of the LLC's capital equals $180,000 when Cory receives his 1/3 capital interest, which of the following tax consequences does not occur in X2?

A)Cory reports $60,000 of ordinary income in X2

B)Adam, Jason and Cory receive an ordinary deduction of $20,000 in X2

C)Adam and Jason receive an ordinary deduction of $30,000 in X2

D)Cory reports $60,000 of ordinary income in X2, and Adam and Jason receive an ordinary deduction of $30,000 in X2

A)Cory reports $60,000 of ordinary income in X2

B)Adam, Jason and Cory receive an ordinary deduction of $20,000 in X2

C)Adam and Jason receive an ordinary deduction of $30,000 in X2

D)Cory reports $60,000 of ordinary income in X2, and Adam and Jason receive an ordinary deduction of $30,000 in X2

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

34

In what order should the tests to determine a partnership's year end be applied?

A)majority interest taxable year - least aggregate deferral - principal partners test.

B)principal partners test - majority interest taxable year - least aggregate deferral.

C)principal partners test - least aggregate deferral - majority interest taxable year.

D)majority interest taxable year - principal partners test - least aggregate deferral.

E)None of these.

A)majority interest taxable year - least aggregate deferral - principal partners test.

B)principal partners test - majority interest taxable year - least aggregate deferral.

C)principal partners test - least aggregate deferral - majority interest taxable year.

D)majority interest taxable year - principal partners test - least aggregate deferral.

E)None of these.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

35

Sue and Andrew form SA general partnership. Each person receives an equal interest in the newly created partnership. Sue contributes $10,000 of cash and land with a FMV of $55,000. Her basis in the land is $20,000. Andrew contributes equipment with a FMV of $12,000 and a building with a FMV of $33,000. His basis in the equipment is $8,000, and his basis in the building is $20,000. How much gain must the SA general partnership recognize on the transfer of these assets from Sue and Andrew?

A)$0

B)$4,000

C)$48,000

D)$52,000

A)$0

B)$4,000

C)$48,000

D)$52,000

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

36

Erica and Brett decide to form their new motorcycle business as an LLC. Each will receive an equal profits (loss) interest by contributing cash, property, or both. In addition to the members' contributions, their LLC will obtain a $50,000 nonrecourse loan from First Bank at the time it is formed. Brett contributes cash of $5,000 and a building he bought as a storefront for the motorcycles. The building has a FMV of $45,000, an adjusted basis of $30,000, and is secured by a $35,000 nonrecourse mortgage that the LLC will assume. What is Brett's outside tax basis in his LLC interest?

A)$37,500

B)$40,000

C)$42,500

D)$45,000

A)$37,500

B)$40,000

C)$42,500

D)$45,000

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

37

A partner's tax basis or at-risk amount can be increased by making capital contributions, by paying off partnership debt, or by increasing the profitability of the partnership.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

38

A partner can apply any passive activity losses against any passive activity income for the year.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

39

Under general circumstances, debt is allocated from the partnership to each partner in the following manner:

A)Recourse - profit sharing ratios; nonrecourse - profit sharing ratios

B)Recourse - capital ratios; nonrecourse - capital ratios

C)Recourse - to partners with the ultimate responsibility for paying the debt; nonrecourse - profit sharing ratios

D)Recourse - profit sharing ratios; nonrecourse - to partners with the ultimate responsibility for paying the debt

A)Recourse - profit sharing ratios; nonrecourse - profit sharing ratios

B)Recourse - capital ratios; nonrecourse - capital ratios

C)Recourse - to partners with the ultimate responsibility for paying the debt; nonrecourse - profit sharing ratios

D)Recourse - profit sharing ratios; nonrecourse - to partners with the ultimate responsibility for paying the debt

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following statements regarding capital and profit interests received for services contributed to a partnership is false?

A)The holding period of a capital or profits interest begins on the date the interest is received

B)Partners receiving capital interests must recognize the liquidation value of their capital interests as capital gain

C)Partners receiving only profits interests generally don't recognize income when the profits interest is received

D)Partners receiving only profits interests include their share of partnership debt in the tax basis of their partnership interest

A)The holding period of a capital or profits interest begins on the date the interest is received

B)Partners receiving capital interests must recognize the liquidation value of their capital interests as capital gain

C)Partners receiving only profits interests generally don't recognize income when the profits interest is received

D)Partners receiving only profits interests include their share of partnership debt in the tax basis of their partnership interest

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

41

What form does a partnership use when filing an annual informational return?

A)Form 1040

B)Form 1041

C)Form 1065

D)Form 1120

A)Form 1040

B)Form 1041

C)Form 1065

D)Form 1120

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

42

Which of the following statements regarding a partner's basis adjustments is true?

A)A partner's basis may never be reduced below zero.

B)A partner must adjust his basis for ordinary income (loss) but not for separately-stated items.

C)A partnership fine or penalty does not affect a partner's basis.

D)Relief of partnership debt increases a partner's tax basis.

A)A partner's basis may never be reduced below zero.

B)A partner must adjust his basis for ordinary income (loss) but not for separately-stated items.

C)A partnership fine or penalty does not affect a partner's basis.

D)Relief of partnership debt increases a partner's tax basis.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

43

Kim received a 1/3 profits and capital interest in Bright Line, LLC in exchange for legal services she provided. In addition to her share of partnership profits or losses, she receives a $30,000 guaranteed payment each year for ongoing services she provides to the LLC. For X4, Bright Line reported the following revenues and expenses: Sales - $150,000, Cost of Goods Sold - $90,000, Depreciation Expense - $45,000, Long-Term Capital Gains - $15,000, Qualified Dividends - $6,000, and Municipal Bond Interest - $3,000. How much ordinary business income (loss) will Bright Line allocate to Kim on her Schedule K-1 for X4?

A)($15,000)

B)$6,000

C)$9,000

D)$15,000

E)None of these will be reported as ordinary business income (loss) on Schedule K-1.

A)($15,000)

B)$6,000

C)$9,000

D)$15,000

E)None of these will be reported as ordinary business income (loss) on Schedule K-1.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

44

Tim, a real estate investor, Ken, a dealer in securities, and Hardware, Inc., a retail lumber store form a partnership called HKT, LP. HKT is in the home building business. Tim recently purchased his interest in HKT while the other partners purchased their interest several years ago. During X3, HKT reports a $12,000 gain from the sale of a stock in a wholesale lumber company it purchased in X1 for investment purposes. Which of the following statements best represents how their portion of the gain should be reported to the partner?

A)Tim - Short-term capital gain

B)Ken - Ordinary Income

C)Hardware, Inc.- Long-term capital gain

D)All of these accurately report the gain to the partner

E)None of these accurately report the gain to the partner

A)Tim - Short-term capital gain

B)Ken - Ordinary Income

C)Hardware, Inc.- Long-term capital gain

D)All of these accurately report the gain to the partner

E)None of these accurately report the gain to the partner

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

45

For partnership tax years ending after December 31, 2015, when must a partnership file its return?

A)By the 15th day of the 3rd month after the partnership's tax year end

B)By the 5th month after the original due date if an extension is filed

C)By the 15th day of the 4th month after the partnership's tax year end

D)By the 15th day of the 3rd month after the partnership's tax year end and by the 5th month after the original due date if an extension is filed

E)By the 5th month after the original due date if an extension is filed and by the 15th day of the 4th month after the partnership's tax year end

A)By the 15th day of the 3rd month after the partnership's tax year end

B)By the 5th month after the original due date if an extension is filed

C)By the 15th day of the 4th month after the partnership's tax year end

D)By the 15th day of the 3rd month after the partnership's tax year end and by the 5th month after the original due date if an extension is filed

E)By the 5th month after the original due date if an extension is filed and by the 15th day of the 4th month after the partnership's tax year end

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following items are subject to the Net Investment Income tax when an individual partner is a material participant in the partnership?

A)Partner's distributive share of dividends

B)Partner's distributive share of interest

C)Partner's distributive share of ordinary business income

D)Both A and B

A)Partner's distributive share of dividends

B)Partner's distributive share of interest

C)Partner's distributive share of ordinary business income

D)Both A and B

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following items are subject to the Net Investment Income tax when a partner is a not a material participant in the partnership?

A)Partner's distributive share of dividends.

B)Partner's distributive share of interest.

C)Partner's distributive share of ordinary business income.

D)All of these are correct.

A)Partner's distributive share of dividends.

B)Partner's distributive share of interest.

C)Partner's distributive share of ordinary business income.

D)All of these are correct.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following would not be classified as a separately-stated item?

A)Short-term capital gains

B)Charitable contributions

C)MACRS depreciation expense

D)Guaranteed payments

A)Short-term capital gains

B)Charitable contributions

C)MACRS depreciation expense

D)Guaranteed payments

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

49

Under proposed regulations issued by the Treasury Department, in which of the following situations should an LLC member be treated as a general partner for self-employment tax purposes?

A)The member is not personally liable for any of the LLC debt.

B)The member has authority to contract on behalf of the LLC.

C)The member spends 450 hours participating in the management of the LLC's trade or business during the taxable year.

D)The member is listed on the LLC's letterheaD.Under proposed regulations, an LLC member should be treated like a general partner for self-employment tax purposes if they are personally liable for any LLC debt, they have authority to contract on behalf of the LLC, or if they participate more than 500 hours in the trade or business of the LLC.

A)The member is not personally liable for any of the LLC debt.

B)The member has authority to contract on behalf of the LLC.

C)The member spends 450 hours participating in the management of the LLC's trade or business during the taxable year.

D)The member is listed on the LLC's letterheaD.Under proposed regulations, an LLC member should be treated like a general partner for self-employment tax purposes if they are personally liable for any LLC debt, they have authority to contract on behalf of the LLC, or if they participate more than 500 hours in the trade or business of the LLC.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

50

On 12/31/X4, Zoom, LLC reported a $60,000 loss on its books. The items included in the loss computation were $30,000 in sales revenue, $15,000 in qualified dividends, $22,000 in cost of goods sold, $50,000 charitable contribution, $20,000 in employee wages, and $13,000 of rent expense. How much ordinary business income (loss) will Zoom report on its X4 return?

A)($8,000)

B)($25,000)

C)($60,000)

D)($95,000)

A)($8,000)

B)($25,000)

C)($60,000)

D)($95,000)

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

51

This year, HPLC, LLC was formed by H Inc., P Inc., L Inc., and C Inc. Each member had an equal share in the LLC's capital. H Inc., P Inc., and L Inc. each had a 30% profits interest in the LLC with C Inc. having a 10% profits interest. The members had the following tax year-ends: H Inc. [1/31], P Inc. [5/31], L Inc. [7/31], and C Inc. [10/31]. What tax year-end must the LLC use?

A)1/31

B)5/31

C)7/31

D)10/31

A)1/31

B)5/31

C)7/31

D)10/31

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

52

Which requirement must be satisfied in order to specially allocate partnership income or losses to partners?

A)Special allocations must have economic effect

B)At least one partner must agree to the special allocations

C)Special allocations must be insignificant

D)Special allocations must reduce the combined tax liability of all the partners

A)Special allocations must have economic effect

B)At least one partner must agree to the special allocations

C)Special allocations must be insignificant

D)Special allocations must reduce the combined tax liability of all the partners

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

53

A partnership may use the cash method despite having a corporate partner when the partnership's average gross receipts for the prior three taxable years don't exceed _________.

A)$500,000

B)$1,000,000

C)$5,000,000

D)Partnerships may never use the cash method if they have corporate partners

A)$500,000

B)$1,000,000

C)$5,000,000

D)Partnerships may never use the cash method if they have corporate partners

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following statements regarding the process for determining a partnership's tax year-end is true?

A)Only the partners' profits interests are relevant when determining if a partnership has a majority interest taxable year.

B)Under the principal partners test, a principal partner is defined as a partner having an interest of 3% or more in the profits or capital of the partnership.

C)The least aggregate deferral test utilizes the partners' capital interests to measure the amount of aggregate deferral.

D)A partnership is required to use a calendar year-end if it has a corporate partner.

E)None of these is true.

A)Only the partners' profits interests are relevant when determining if a partnership has a majority interest taxable year.

B)Under the principal partners test, a principal partner is defined as a partner having an interest of 3% or more in the profits or capital of the partnership.

C)The least aggregate deferral test utilizes the partners' capital interests to measure the amount of aggregate deferral.

D)A partnership is required to use a calendar year-end if it has a corporate partner.

E)None of these is true.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

55

A partner's self-employment earnings (loss) may be affected by her share of ordinary business income (loss) and any guaranteed payments she receives. The impact of these amounts typically depends on the status of the partner. Which of the following statements correctly describes the effect these items have on the partner's self-employment earnings (loss)?

A)General partner - only guaranteed payments affect self-employment earnings (loss)

B)General partner - ordinary business income (loss) and guaranteed payments affect self-employment earnings (loss)

C)Limited partner - only guaranteed payments affect self-employment earnings (loss)

D)Limited partner - only ordinary business income (loss) affects self-employment income (loss)

E)Both B and C

A)General partner - only guaranteed payments affect self-employment earnings (loss)

B)General partner - ordinary business income (loss) and guaranteed payments affect self-employment earnings (loss)

C)Limited partner - only guaranteed payments affect self-employment earnings (loss)

D)Limited partner - only ordinary business income (loss) affects self-employment income (loss)

E)Both B and C

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

56

Frank and Bob are equal members in Soxy Socks, LLC. When forming the LLC, Frank contributed $50,000 in cash and $50,000 worth of equipment. Frank's adjusted basis in the equipment was $35,000. Bob contributed $50,000 in cash and $50,000 worth of land. Bob's adjusted basis in the land was $30,000. On 3/15/X4, Soxy Socks sells the land Bob contributed for $60,000. How much gain (loss) related to this transaction will Bob report on his X4 return?

A)$10,000

B)$15,000

C)$25,000

D)$35,000

A)$10,000

B)$15,000

C)$25,000

D)$35,000

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

57

TQK, LLC provides consulting services and was formed on 1/31/X5. Aaron and ABC, Inc. each hold a 50% capital and profits interest in TQK. If TQK averaged $7,000,000 in annual gross receipts over the last three years, what accounting method can TQK use for X9?

A)Accrual method

B)Cash method

C)Hybrid method

D)Accrual method or Cash method

A)Accrual method

B)Cash method

C)Hybrid method

D)Accrual method or Cash method

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

58

What is the rationale for the specific rules partnerships must follow in determining a partnership's taxable year-end?

A)To increase the amount of aggregate tax deferral partners receive

B)To minimize the amount of aggregate tax deferral partners receive

C)To align the year-end of the partnership with the year-end of a majority of the partners

D)To spread the workload of CPAs more evenly over the year

E)Both B and C

A)To increase the amount of aggregate tax deferral partners receive

B)To minimize the amount of aggregate tax deferral partners receive

C)To align the year-end of the partnership with the year-end of a majority of the partners

D)To spread the workload of CPAs more evenly over the year

E)Both B and C

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

59

What is the correct order for applying the following three items to adjust a partner's tax basis in his partnership interest: (1) Increase for share of ordinary business income, (2) Decrease for share of separately stated loss items, and (3) Decrease for distributions?

A)1, 3, 2

B)1, 2, 3

C)3, 1, 2

D)2, 3, 1

A)1, 3, 2

B)1, 2, 3

C)3, 1, 2

D)2, 3, 1

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following does not adjust a partner's basis?

A)Ordinary business income (loss)

B)Change in amount of partnership debt

C)Tax-exempt income

D)All of these adjust a partner's basis

A)Ordinary business income (loss)

B)Change in amount of partnership debt

C)Tax-exempt income

D)All of these adjust a partner's basis

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

61

On January 1, X9, Gerald received his 50% profits and capital interest in High Air, LLC in exchange for $2,000 in cash and real property with a $3,000 tax basis secured by a $2,000 nonrecourse mortgage. High Air reported a $15,000 loss for its X9 calendar year. How much loss can Gerald deduct, and how much loss must he suspend if he only applies the tax basis loss limitation?

A)$0, $4,000

B)$0, $7,500

C)$0, $15,000

D)$4,000, $0

E)None of these

A)$0, $4,000

B)$0, $7,500

C)$0, $15,000

D)$4,000, $0

E)None of these

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

62

How does additional debt or relief of debt affect a partner's basis?

A)Debt has no effect on a partner's basis

B)Relief of debt increases a partner's basis

C)Both additional debt and relief of debt increase a partner's basis

D)Additional debt increases a partner's basis

A)Debt has no effect on a partner's basis

B)Relief of debt increases a partner's basis

C)Both additional debt and relief of debt increase a partner's basis

D)Additional debt increases a partner's basis

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

63

Jay has a tax basis of $14,000 in his partnership interest at the beginning of the partnership tax year. The following amounts of partnership debt were allocated to Jay and are included in his beginning of the year tax basis: (1) recourse debt - $3,000, (2) qualified nonrecourse debt - $1,000, and (3) nonrecourse debt - $500. If Jay is allocated a $15,000 loss for the current year, how much of the loss will be suspended under the tax basis and at-risk limitations?

A)$500, $1,000

B)$1,000, $500

C)$0, $0

D)$14,000, $1,000

A)$500, $1,000

B)$1,000, $500

C)$0, $0

D)$14,000, $1,000

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

64

Jerry, a partner with 30% capital and profit interest, received his Schedule K-1 from Plush Pillows, LP. At the beginning of the year, Jerry's tax basis in his partnership interest was $50,000. His current year Schedule K-1 reported an ordinary loss of $15,000, long-term capital gain of $3,000, qualified dividends of $2,000, $500 of non-deductible expenses, a $10,000 cash contribution, and a reduction of $4,000 in his share of partnership debt. What is Jerry's adjusted basis in his partnership interest at the end of the year?

A)$35,000

B)$40,000

C)$45,500

D)$49,500

A)$35,000

B)$40,000

C)$45,500

D)$49,500

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

65

If a taxpayer sells a passive activity with suspended passive activity losses from prior years, what type of income can be offset by the suspended passive losses in the year of sale?

A)Passive activity income

B)Portfolio income

C)Active business income

D)Any of these types of income can be offset.

E)None of these.

A)Passive activity income

B)Portfolio income

C)Active business income

D)Any of these types of income can be offset.

E)None of these.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

66

In what order are the loss limitations for partnerships applied?

A)Tax Basis - At-Risk Amount - Passive Activity Loss

B)Passive Activity Loss - Tax Basis - At-Risk Amount

C)Tax Basis - Passive Activity Loss - At-Risk Amount

D)At-Risk Amount - Tax Basis - Passive Activity Loss

A)Tax Basis - At-Risk Amount - Passive Activity Loss

B)Passive Activity Loss - Tax Basis - At-Risk Amount

C)Tax Basis - Passive Activity Loss - At-Risk Amount

D)At-Risk Amount - Tax Basis - Passive Activity Loss

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following would not be classified as a material participant in an activity?

A)An individual who participates more than 100 hours a year and the person's participation is not less than any other individual's participation

B)An individual who participated in the activity for at least one of the preceding five taxable years

C)An individual who participates in an activity regularly, continuously, and substantially

D)An individual who participates in an activity for more than 500 hours a year

A)An individual who participates more than 100 hours a year and the person's participation is not less than any other individual's participation

B)An individual who participated in the activity for at least one of the preceding five taxable years

C)An individual who participates in an activity regularly, continuously, and substantially

D)An individual who participates in an activity for more than 500 hours a year

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

68

Hilary had an outside basis in LTL, General Partnership of $10,000 at the beginning of the year. LTL reported the following items on Hilary's K-1 for the year: ordinary business income of $5,000, a $10,000 reduction in Hilary's share of partnership debt, a cash distribution of $20,000, and tax-exempt income of $3,000. What is Hilary's adjusted basis at the end of the year?

A)($12,000)

B)($9,000)

C)$0

D)$15,000

E)$18,000

A)($12,000)

B)($9,000)

C)$0

D)$15,000

E)$18,000

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

69

What type of debt is not included in calculating a partner's at-risk amount?

A)Recourse debt

B)Qualified nonrecourse debt

C)Nonrecourse debt

D)All of these types of debt are included in the at-risk amount

A)Recourse debt

B)Qualified nonrecourse debt

C)Nonrecourse debt

D)All of these types of debt are included in the at-risk amount

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

70

On March 15, 20X9, Troy, Peter, and Sarah formed Picture Perfect general partnership. This partnership was created to sell a variety of cameras, picture frames, and other photography accessories. When it was formed, the partners received equal profits and capital interests and the following items were contributed by each partner:

• Troy - cash of $3,000, inventory with a FMV and tax basis of $5,000, and a building with a FMV of $22,000 and adjusted basis of $10,000. Additionally, the building was secured by a $10,000 nonrecourse mortgage.

• Peter - cash of $5,000, accounts payable of $12,000 (recourse debt for which each partner becomes equally responsible), and land with a FMV of $27,000 and tax basis of $20,000.

• Sarah - cash of $2,000, accounts receivable with a FMV and tax basis of $1,000, and equipment with a FMV of $40,000 and adjusted basis of $3,500. Sarah also contributed a $23,000 nonrecourse note payable secured by the equipment.

What is each partner's outside basis and how much gain (loss) must the partners recognize in 20X9 when Picture Perfect was formed?

• Troy - cash of $3,000, inventory with a FMV and tax basis of $5,000, and a building with a FMV of $22,000 and adjusted basis of $10,000. Additionally, the building was secured by a $10,000 nonrecourse mortgage.

• Peter - cash of $5,000, accounts payable of $12,000 (recourse debt for which each partner becomes equally responsible), and land with a FMV of $27,000 and tax basis of $20,000.

• Sarah - cash of $2,000, accounts receivable with a FMV and tax basis of $1,000, and equipment with a FMV of $40,000 and adjusted basis of $3,500. Sarah also contributed a $23,000 nonrecourse note payable secured by the equipment.

What is each partner's outside basis and how much gain (loss) must the partners recognize in 20X9 when Picture Perfect was formed?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

71

What is the difference between the aggregate and entity theory of partnership taxation? Provide two examples of how partnership tax rules reflect the aggregate theory and two examples of how they reflect the entity theory.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following statements regarding partnerships losses suspended by the tax basis limitation is true?

A)Partnership losses must be used only in the year the losses are created

B)Partnership losses may be carried back 2 years and carried forward 5 years

C)Partnership losses may be carried forward indefinitely

D)Partnership losses may be carried back 2 years and carried forward 20 years

A)Partnership losses must be used only in the year the losses are created

B)Partnership losses may be carried back 2 years and carried forward 5 years

C)Partnership losses may be carried forward indefinitely

D)Partnership losses may be carried back 2 years and carried forward 20 years

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following statements regarding the rationale for adjusting a partner's basis is false?

A)To prevent partners from being double taxed when they sell their partnership interests

B)To ensure that partnership tax-exempt income is not ultimately taxed

C)To prevent partners from being double taxed when they receive cash distributions

D)To ensure that partnership non-deductible expenses are never deductible

E)None of these rationales are false

A)To prevent partners from being double taxed when they sell their partnership interests

B)To ensure that partnership tax-exempt income is not ultimately taxed

C)To prevent partners from being double taxed when they receive cash distributions

D)To ensure that partnership non-deductible expenses are never deductible

E)None of these rationales are false

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

74

Styling Shoes, LLC filed its 20X8 Form 1065 on March 15, 20X9. Styling had three members with the following ownership interests and tax basis at the beginning of the 20X8: (1) Jane, a member with a 25% profits and capital interest and a $5,000 outside basis, (2) Joe, a member with a 45% profits and capital interest and a $10,000 outside basis, and (3) Jack, a member with a 30% profits and capital interest and a $2,000 outside basis. The following items were reported on Styling's Schedule K for the year: ordinary income of $100,000, Section 1231 gain of $15,000, charitable contributions of $25,000, and tax-exempt income of $3,000. In addition, Styling received an additional bank loan of $12,000 during 20X8. What is Jane's tax basis after adjustment for her share of these items?

A)$28,250

B)$31,250

C)$33,500

D)$57,250

A)$28,250

B)$31,250

C)$33,500

D)$57,250

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

75

John, a limited partner of Candy Apple, LP, is allocated $30,000 of ordinary business loss from the partnership. Before the loss allocation, his tax basis is $20,000 and at-risk amount is $10,000. John also has ordinary business income of $20,000 from Sweet Pea, LP as a general partner and ordinary business income of $5,000 from Red Tomato, as a limited partner. How much of the $30,000 loss from Candy Apple can John deduct currently?

A)$5,000

B)$10,000

C)$25,000

D)$30,000

A)$5,000

B)$10,000

C)$25,000

D)$30,000

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

76

Which person would generally be treated as a material participant in an activity?

A)A participant in a rental activity

B)A limited partner

C)A LLC member not involved with management of the LLC

D)A general partner

A)A participant in a rental activity

B)A limited partner

C)A LLC member not involved with management of the LLC

D)A general partner

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

77

Does adjusting a partner's basis for tax-exempt income prevent double taxation?

A)Yes, if this basis adjustment is not made the partner will be taxed once when the income is allocated to him and a second time when he sells his partnership interest

B)Yes, if this basis adjustment is not made the partner will be taxed on the tax-exempt income twice when he sells his partnership interest because he was not taxed on this income when it was earned

C)No, making this adjustment to the partner's basis prevents the tax-exempt income from being converted to taxable income

D)No, the partner should not adjust his tax basis by his share of tax-exempt income

A)Yes, if this basis adjustment is not made the partner will be taxed once when the income is allocated to him and a second time when he sells his partnership interest

B)Yes, if this basis adjustment is not made the partner will be taxed on the tax-exempt income twice when he sells his partnership interest because he was not taxed on this income when it was earned

C)No, making this adjustment to the partner's basis prevents the tax-exempt income from being converted to taxable income

D)No, the partner should not adjust his tax basis by his share of tax-exempt income

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following items will affect a partner's tax basis?

A)Share of ordinary business income (loss)

B)Share of nonrecourse debt

C)Share of recourse debt

D)Share of qualified nonrecourse debt

E)All of these will affect a partner's tax basis

A)Share of ordinary business income (loss)

B)Share of nonrecourse debt

C)Share of recourse debt

D)Share of qualified nonrecourse debt

E)All of these will affect a partner's tax basis

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

79

If partnership debt is reduced and a partner is deemed to receive a cash distribution, what impact does the deemed distribution have on the partner if it is in excess of her tax basis?

A)The partner will treat the distribution in excess of her basis as ordinary income

B)The partner will treat the distribution in excess of her basis as capital gain

C)The partner will not ever be taxed on the distribution in excess of her basis

D)The partner will not be taxed on the distribution in excess of her basis until she sells her partnership interest

A)The partner will treat the distribution in excess of her basis as ordinary income

B)The partner will treat the distribution in excess of her basis as capital gain

C)The partner will not ever be taxed on the distribution in excess of her basis

D)The partner will not be taxed on the distribution in excess of her basis until she sells her partnership interest

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

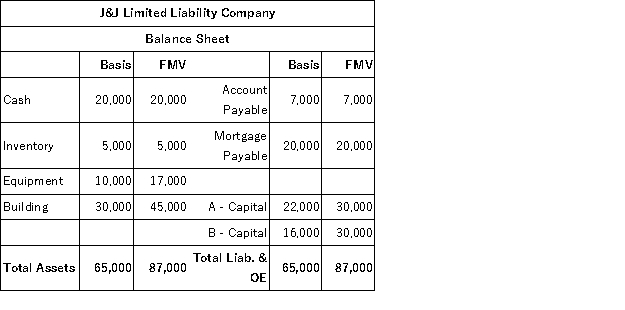

80

J&J, LLC was in its third year of operations when J&J decided to expand the number of members from two, A & B, with equal profits and capital interests to three members, A, B, and

C.The third member, C, will contribute her financial expertise to the LLC in exchange for a 1/3 capital interest in J&J.Given the balance sheet below reflecting the financial position of J&J on the date member C is admitted, what are the tax consequences to members A, B, and C, and to J&J when C receives her capital interest? If, instead, member C receives a 1/3 profit interest, what would be the tax consequences to members A, B, and C, and to J&J?

C.The third member, C, will contribute her financial expertise to the LLC in exchange for a 1/3 capital interest in J&J.Given the balance sheet below reflecting the financial position of J&J on the date member C is admitted, what are the tax consequences to members A, B, and C, and to J&J when C receives her capital interest? If, instead, member C receives a 1/3 profit interest, what would be the tax consequences to members A, B, and C, and to J&J?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 100 flashcards in this deck.