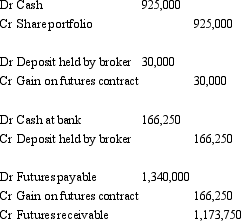

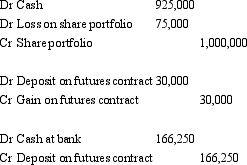

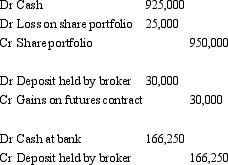

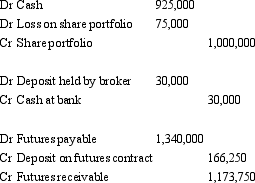

Partridge Ltd holds a well-diversified portfolio of shares with a current market value on 1 April 2004 of $1 million. On this date Partridge Ltd decides to hedge the portfolio by taking a sell position in fifteen SPI futures units. The All Ordinaries SPI is 3,130 on 1 April 2004. A unit contract in SPI futures is priced based on All Ordinaries SPI and a price of $25. The futures broker requires a deposit of $80,000. On 30 June the All Ordinaries SPI has fallen to 2,980 and the value of the company's share portfolio has fallen to $950,000. On 1 July 2004 Partridge Ltd decides to sell its shares and close out its futures contract. At this date the portfolio has a market value of $925,000 and the All Ordinaries SPI is 2,900. Assume all entries have been made to mark to market the futures contract and record changes in the deposit up to 1 July. What are the entries to record the transactions of 1 July 2004 (only)?

A.

B.

C.

D.

E. None of the given answers.

Correct Answer:

Verified

Q9: The central issue in classifying a financial

Q10: For a designated cash flow hedge,AASB 139

Q15: Under AASB 139,an entity is required to

Q23: The market price of an option is

Q25: Penitent Ltd acquired a parcel of 10,000

Q26: Jackson Ltd has a US$50, 000 receivable

Q27: Which of the following are examples of

Q33: According to AASB 132,which of the following

Q34: The characteristics of a swap agreement may

Q36: What is hedging?

A. It is a method

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents