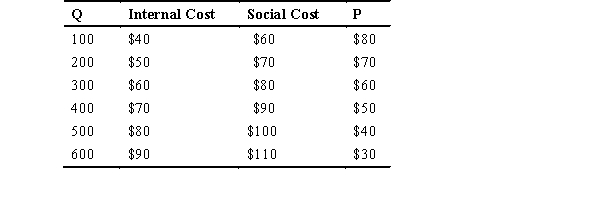

Refer to the accompanying table,where Q represents the quantity produced,internal cost and social cost are given for various quantities,and P represents the price consumers are willing to pay for various quantities,to answer the following questions.

-The market equilibrium occurs where price is ________ and quantity is ________.

A) $70; 200

B) $50; 200

C) $60; 300

D) $80; 300

E) $60; 100

Correct Answer:

Verified

Q14: Suzanne drives to work each day.The best

Q15: External costs are the result of the

Q16: The amount an individual pays for gasoline

Q17: The amount an individual pays for insurance

Q18: The costs of a market activity paid

Q20: The personal decisions of consumers and firms

Q21: If government regulation forces firms in an

Q22: Consider the market for refined oil.In the

Q23: Consider a market where production of a

Q24: Consider a market with a negative externality.The

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents