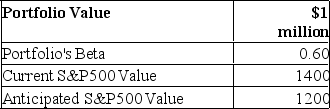

You are given the following information about a portfolio you are to manage.For the long term, you are bullish, but you think the market may fall over the next month.  If the anticipated market value materializes, what will be your expected loss on the portfolio?

If the anticipated market value materializes, what will be your expected loss on the portfolio?

A) 14.29%

B) 16.67%

C) 15.43%

D) 8.57%

Correct Answer:

Verified

Q22: Suppose that the risk-free rates in the

Q23: Suppose that the risk-free rates in the

Q24: The value of a futures contract for

Q24: You are given the following information about

Q26: Which two indices had the highest correlation

Q28: You are given the following information about

Q29: If you sold an S&P 500 Index

Q30: Commodity futures pricing

A)must be related to spot

Q32: Suppose that the risk-free rates in the

Q39: Trading in stock index futures

A) now exceeds

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents