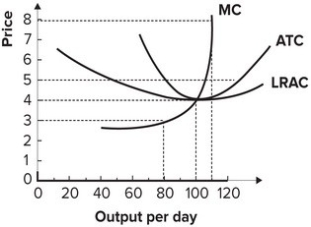

Refer to the graph shown, which depicts a perfectly competitive firm. When the industry is in long-run competitive equilibrium:

A) the price of the product will be $6.

B) the firm will produce 100 units of output.

C) the firm will earn economic profits of $300 per day.

D) the marginal cost of production will be $3.

Correct Answer:

Verified

Q109: The long-run industry supply curve will be

Q110: Refer to the graph shown, which depicts

Q111: Suppose the minimum possible price of constructing

Q112: Suppose that the marginal cost of producing

Q113: During a recession, the price of restaurant

Q115: If the long-run market supply curve is

Q116: Assume that the t-shirt industry is perfectly

Q117: Many fast-food restaurants have begun offering value

Q118: Long-run competitive equilibrium requires:

A) average costs to

Q119: The existence of economic losses induces firms

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents