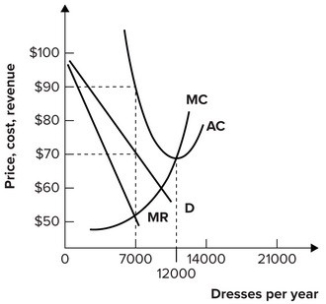

Refer to the graph shown of a monopolistically competitive firm. In the long run:

A) marginal cost will fall for firms that remain as other firms exit the industry.

B) average total cost will rise for firms that remain as other firms enter the industry.

C) demand will fall for firms that remain as other firms enter the industry.

D) demand will rise for firms that remain as other firms exit the industry.

Correct Answer:

Verified

Q183: In the long-run equilibrium for a monopolistically

Q193: Refer to the graph shown of a

Q194: Refer to the graph shown. The equilibrium

Q197: Refer to the graph shown. The monopolistically

Q199: Refer to the graph shown. The short-run

Q199: Under monopolistic competition, a firm's ability to

Q200: Under monopolistic competition, a long-run equilibrium exists

Q201: Refer to the graph shown depicting a

Q205: The difference between a monopolist and a

Q211: Suppose marginal cost is constant and equal

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents