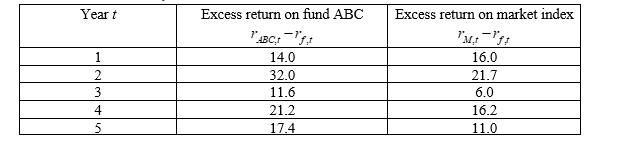

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-Given the data in question 6, what is the estimated beta (  ) of Fund ABC?

) of Fund ABC?

A) 3.1

B) 2.1

C) 1.1

D) None of the above

Correct Answer:

Verified

Q9: Which of the following is NOT correct

Q10: Which of the following is NOT a

Q11: Suppose you have 5-year annual data on

Q12: The type I error associated with testing

Q13: Which of these is not a reason

Q15: Suppose you have 5-year annual data on

Q16: In a time series regression of

Q17: Which of the following is a correct

Q18: The method of estimating econometric models which

Q19: Suppose you have 5-year annual data on

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents