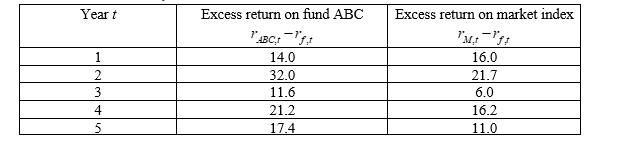

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-Suppose that the unbiased estimator of the standard deviation of the disturbance (s) is 5.1. What is the nearest value to the standard errors of the estimated CAPM alpha (  ) of Fund ABC from question 6?

) of Fund ABC from question 6?

A) 3.5

B) 4.5

C) 5.5

D) 6.5

Correct Answer:

Verified

Q1: Assuming there are 1000 observations in your

Q2: Consider a bivariate regression model with coefficient

Q3: What result is proved by the Gauss-Markov

Q5: Regression is concerned with describing and evaluating

Q6: Suppose you have calculated the following regression

Q7: Which of the following statements is correct

Q8: What does a positive linear relationship between

Q9: Which of the following is NOT correct

Q10: Which of the following is NOT a

Q11: Suppose you have 5-year annual data on

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents