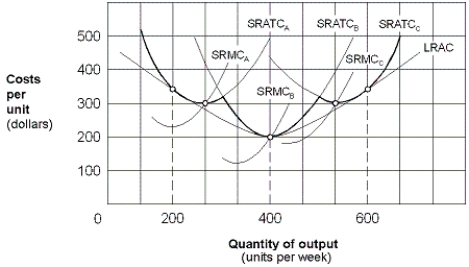

Exhibit 8-18 A typical firm in a perfectly competitive market

-In Exhibit 8-18, assume the perfectly competitive firm is in long-run equilibrium and there is an increase in demand. As a result, the firm in the short run will increase output along its:

A) short-run average total cost curve B.

B) short-run marginal cost curve B.

C) long-run average cost curve.

D) none of these because the firm shuts down.

Correct Answer:

Verified

Q107: If the expansion of output in an

Q156: If resource prices rise and the per-unit

Q192: Consider a firm operating with the following:

Q193: Assume the short-run average total cost for

Q194: The long-run supply curve for a competitive

Q197: Exhibit 8-18 A typical firm in a

Q198: Which of the following is true of

Q199: In a constant-cost industry, input prices remain

Q200: If a perfectly competitive industry's long-run supply

Q201: Exhibit 8-19 Long-run perfectly competitive industry

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents