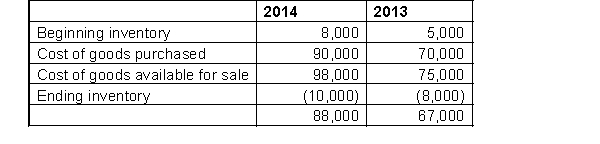

Winston Auto Parts reported the following information in its income statement for 2013 and 2014:  Additional Information:

Additional Information:  While completing Winston's 2015 financial statements, the accountant realized that errors had been made in previous years' inventory calculations. The correct ending inventory at December 31, 2012 was $6,000, the correct ending inventory at December 31, 2013 was $4,000, and the correct ending inventory at December 31, 2014 was $7,000.

While completing Winston's 2015 financial statements, the accountant realized that errors had been made in previous years' inventory calculations. The correct ending inventory at December 31, 2012 was $6,000, the correct ending inventory at December 31, 2013 was $4,000, and the correct ending inventory at December 31, 2014 was $7,000.

Instructions

a. Calculate the correct cost of goods sold and gross profit for 2013 and for 2014.

b. Calculate the inventory turnover for 2013 and 2014:

(i) using the originally reported information; and

(ii) using the corrected information.

c. Calculate the gross profit margin for 2013 and 2014:

(i) using the originally reported information; and

(ii) using the corrected information.

d. Explain how the errors will have caused management performance to be improperly evaluated.

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q147: O'Meara Sales sells golf bags and uses

Q148: Fyodorov Company, using a periodic inventory system,

Q149: Bermuda Beach Boutique Company uses a perpetual

Q150: O'Neil's Hardware Store, in St. John's, NL,

Q151: For each of the independent events listed

Q153: Chan Pharmacy reported cost of goods sold

Q154: Hamil Company prepares monthly financial statements and

Q155: Walters Department Store uses the retail inventory

Q156: Windsor Company reported the following summarized information

Q157: Labco Company reported the following partial income

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents