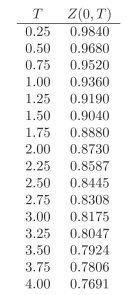

Use the following discount factors when needed.

-Calculate the convexity of the following portfolio:

i. 2 units of a 1.5-year ?xed rate bond paying 6% quarterly.

ii. 4 units of a 1.75-year ?oating rate bond paying ?oat + 80 bps semi- annually. You know that the reference rate was 7% three months ago. 13

iii. 6 units of a 2-year zero coupon bond.

iv. 1 units of a 1.5-year ?oating rate bond with no spread paid semian- nually.

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q8: What is the advantage of a factor

Q9: Use the following discount factors when needed.

Q10: You currently hold a 7-year ?xed rate

Q11: Use the following discount factors when needed.

Q12: Suppose you hold a bond and interest

Q13: Compute the Term Spread and the Butterfly

Q14: Use the following discount factors when needed.

Q15: Suppose you hold a bond and interest

Q16: Compute the Term Spread and the Butterfly

Q18: Compute the Term Spread and the Butter?y

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents