SCENARIO 16-13

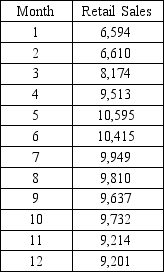

Given below is the monthly time series data for U.S.retail sales of building materials over a specific year.

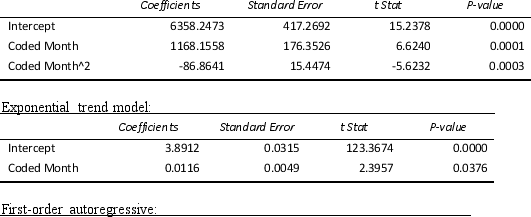

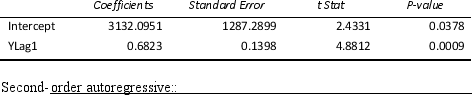

The results of the linear trend,quadratic trend,exponential trend,first-order autoregressive,second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the 1st month is 0:

The results of the linear trend,quadratic trend,exponential trend,first-order autoregressive,second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the 1st month is 0:

Linear trend model:

Quadratic trend model:

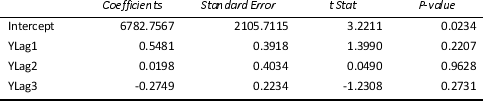

Third-order autoregressive::

Third-order autoregressive::

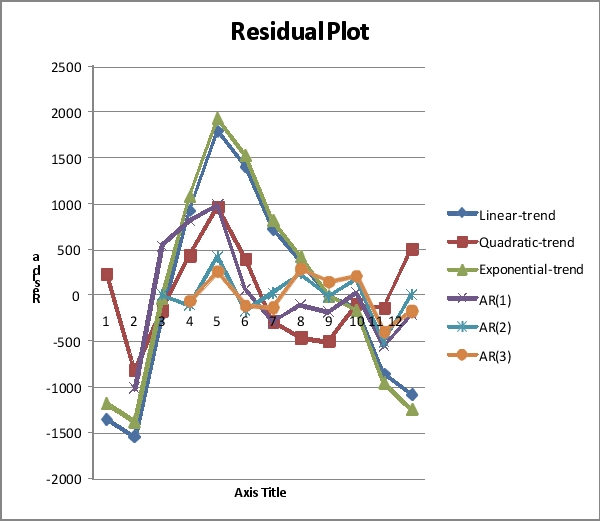

Below is the residual plot of the various models:

-Referring to Scenario 16-13,what is the exponentially smoothed value for the first month using a smoothing coefficient of W = 0.5?

Correct Answer:

Verified

Q122: SCENARIO 16-13

Given below is the monthly time

Q123: SCENARIO 16-13

Given below is the monthly time

Q124: SCENARIO 16-13

Given below is the monthly time

Q125: SCENARIO 16-13

Given below is the monthly time

Q126: SCENARIO 16-13

Given below is the monthly time

Q128: SCENARIO 16-13

Given below is the monthly time

Q129: SCENARIO 16-13

Given below is the monthly time

Q130: SCENARIO 16-12

A local store developed a multiplicative

Q131: SCENARIO 16-13

Given below is the monthly time

Q132: SCENARIO 16-13

Given below is the monthly time

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents