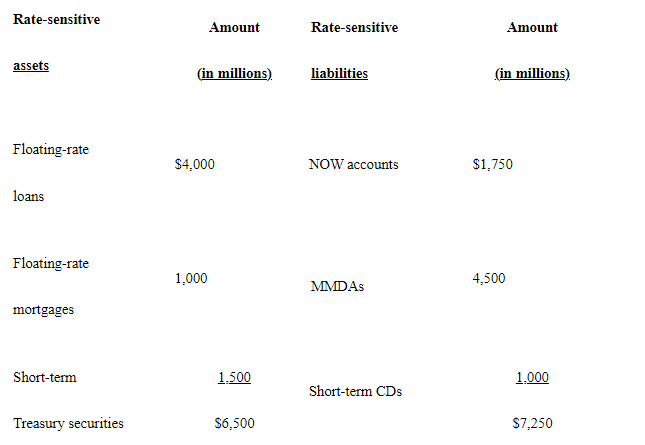

A bank has the following asset and liability portfolios. What is the gap?

A) $750 million

B) - $750 million

C) 1.12

D) .896

E) None of these are correct.

Correct Answer:

Verified

Q28: Banks tend to focus their loans in

Q29: A bank has a return on assets

Q30: Banks can increase their potential interest revenues

Q31: If a bank sells interest rate futures,

Q32: Banks can improve their liquidity position by

Q34: If Bank A has a negative gap

Q35: A common method for banks to reduce

Q36: A bank's net interest margin is commonly

Q37: ROE is defined as Q38: Banks can reduce their credit risk by

A) ![]()

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents