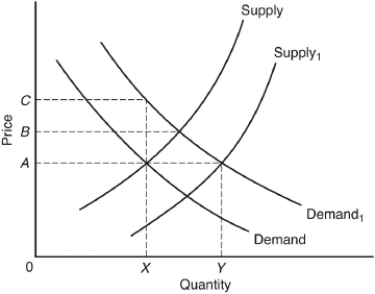

The following question are based on the following graph, showing short-run supply and demand curves for a perfectly competitive market. The initial supply curve is labeled "Supply" and the initial demand curve is labeled "Demand." Price 0A and output rate 0X represent the initial equilibrium price and output.

-The typical producer in this market

A) faces a demand curve less elastic than the one shown.

B) minimizes total cost.

C) produces a tiny fraction of output 0X.

D) must produce at least 0Y.

E) must increase price to break even.

Correct Answer:

Verified

Q51: Q52: The basic distinction between the short run Q53: The following question are based on the Q54: Perfectly competitive firms have zero economic profits Q55: In the long run,what adjustments take place Q57: The market supply curve for a perfectly Q58: The following question are based on the Q59: Under perfect competition,the existence of economic profits Q60: If price equals average total cost,economic profit Q61: Shortages typically arise when there are![]()

A) price

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents