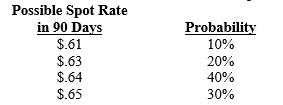

Assume that Kramer Co. will receive SF800,000 in 90 days. Today's spot rate of the Swiss franc is $.62, and the 90-day forward rate is $.635. Kramer has developed the following probability distribution for the spot rate in 90 days:

The probability that the forward hedge will result in more dollars received than not hedging is:

A) 10 percent.

B) 20 percent.

C) 30 percent.

D) 50 percent.

E) 70 percent.

Correct Answer:

Verified

Q9: Spears Co. will receive SF1,000,000 in 30

Q11: Assume the following information:

U.S. deposit rate for

Q12: Which of the following reflects a hedge

Q13: An example of cross-hedging is:

A)find two currencies

Q15: If interest rate parity exists and transaction

Q16: Assume that Patton Co. will receive 100,000

Q17: Money Corp. frequently uses a forward hedge

Q53: From the perspective of Detroit Co., which

Q54: Assume zero transaction costs. If the 90-day

Q71: Assume that Smith Corp. will need to

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents