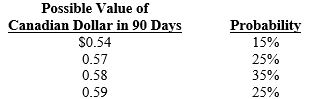

Lorre Co. needs 200,000 Canadian dollars (C$) in 90 days and is trying to determine whether or not to hedge this position. Lorre has developed the following probability distribution for the Canadian dollar:

The 90-day forward rate of the Canadian dollar is $.575, and the expected spot rate of the Canadian dollar in 90 days is $.55. If Lorre implements a forward hedge, what is the probability that hedging will be more costly to the firm than not hedging?

A) 40 percent

B) 60 percent

C) 15 percent

D) 85 percent

Correct Answer:

Verified

Q14: If interest rate parity exists, the forward

Q20: The real cost of hedging payables in

Q32: Exhibit 11-1 Q33: Since the results of both a money Q34: You are the treasurer of Arizona Corp. Q37: To hedge a contingent exposure, in which

![]()

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents