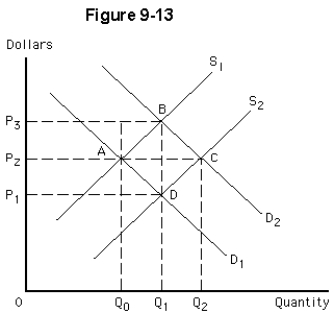

-Assume the initial equilibrium is at point D in Figure 9-13.If the market demand curve shifts from D₁ to D₂,and this results in entry of new firms in the long-run,the new equilibrium in this increasing-cost industry will be

A) both C and E

B) both D and E

C) at a price less than P₁

D) at a price higher than P₁

E) at an output greater than Q₁

Correct Answer:

Verified

Q177: In a perfectly competitive,decreasing-cost industry,the long-run market

Q178: In the long run in a competitive

Q179: If price exceeds average total cost in

Q180: Assume that a constant-cost,perfectly competitive market is

Q181: If expansion of an industry's output causes

Q183: In an increasing-cost industry,the long-run market supply

Q184: In a decreasing-cost industry,the long-run industry supply

Q185: In a market economy,the main market signal

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents