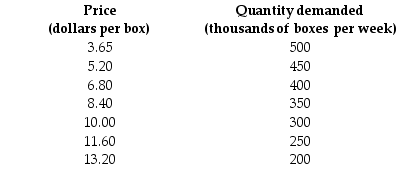

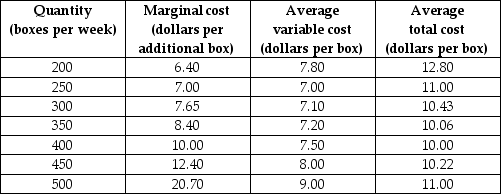

Use the table below to answer the following question.

Table 12.4.1

-Refer to Table 12.4.1. The top table shows the market demand schedule for paper. The market is perfectly competitive and there are 1,000 firms that produce paper. Each firm has the costs shown in the bottom table when it uses its least-cost plant. The market price in the long run is ________ a box and the equilibrium quantity produced in the long run is ________ boxes a week.

A) $11.60; 250,000

B) $7.00; a little less than 400,000

C) $10.00; 300,000

D) $6.40; a little more than 400,000

E) $8.40; 350,000

Correct Answer:

Verified

Q81: When a perfectly competitive market is in

Q85: Firms will stop exiting a market only

Q86: Use the figure below to answer the

Q87: Use the information below to answer the

Q88: Which one of the following does not

Q91: Use the figure below to answer the

Q92: Use the figure below to answer the

Q95: Suppose that the market in which bakeries

Q96: If firms exit an market,the

A)market supply curve

Q100: If firms in a perfectly competitive market

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents