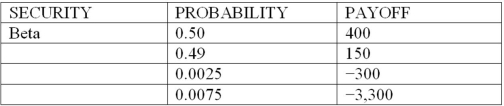

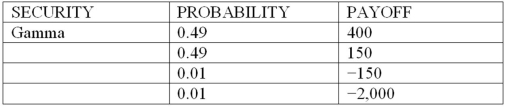

Consider the following discrete probability distributions of payoffs for 3 securities that are held in a DI's trading portfolio (payoff amounts shown are in $millions) :

What are the expected returns for securities Alpha and Beta, respectively (in millions) ?

What are the expected returns for securities Alpha and Beta, respectively (in millions) ?

A) -$248 and + 248

B) +$248 and +$248

C) -$300 and +$400

D) +$300 and - $3,300

E) none of these

Correct Answer:

Verified

Q85: Sumitomo Bank's risk manager has estimated that

Q86: Consider the following discrete probability distributions of

Q87: Sumitomo Bank's risk manager has estimated that

Q88: On December 31, 2001 Historic Bank had

Q91: Sumitomo Bank's risk manager has estimated that

Q92: Sumitomo Bank's risk manager has estimated that

Q92: Sumitomo Bank's risk manager has estimated that

Q93: Consider the following discrete probability distributions of

Q94: City bank has six-year zero coupon bonds

Q95: Sumitomo Bank's risk manager has estimated that

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents