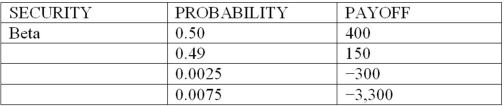

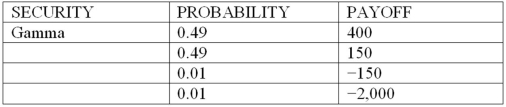

Consider the following discrete probability distributions of payoffs for 3 securities that are held in a DI's trading portfolio (payoff amounts shown are in $millions) :

Based on your answers to the previous three questions, which of the following is true?

Based on your answers to the previous three questions, which of the following is true?

A) Security Alpha represents the riskier of the two assets in the trading portfolio because there is a one-percent probability of loss the following day.

B) Both securities have the same expected payoff; therefore, it makes no difference which is in the trading portfolio.

C) Security Beta is the better asset to have in the trading portfolio since there is a 50 percent probability of a $400 payoff versus only $355 with security Alpha.

D) Both securities have the same expected payoff and value at risk (VAR) , therefore it makes no difference which is in the trading portfolio.

E) According to the expected shortfall measure, if tomorrow is a bad trading day, losses will exceed $25 million.

Correct Answer:

Verified

Q68: Considering the Capital Asset Pricing Model, which

Q69: If a stock portfolio replicates the returns

Q81: On December 31, 2001 Historic Bank had

Q82: On December 31, 2001 Historic Bank had

Q84: The mean change in the value of

Q84: Consider the following discrete probability distributions of

Q85: Sumitomo Bank's risk manager has estimated that

Q86: Consider the following discrete probability distributions of

Q87: Sumitomo Bank's risk manager has estimated that

Q88: On December 31, 2001 Historic Bank had

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents