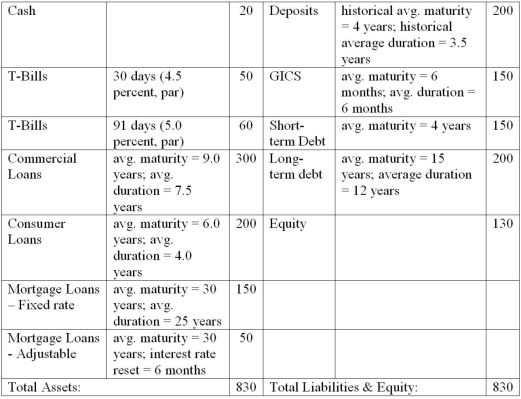

The numbers provided are in millions of dollars and reflect market values:  A risk manager could restructure assets and liabilities to reduce interest rate exposure for this example by

A risk manager could restructure assets and liabilities to reduce interest rate exposure for this example by

A) increasing the average duration of its assets to 9.56 years.

B) decreasing the average duration of its assets to 4.00 years.

C) increasing the average duration of its liabilities to 6.78 years.

D) increasing the average duration of its liabilities to 9.782 years.

E) increasing the leverage ratio, k, to 1.

Correct Answer:

Verified

Q106: The numbers provided are in millions of

Q108: The numbers provided are in millions of

Q109: A bond is scheduled to mature in

Q110: U.S. Treasury quotes from the WSJ on

Q111: The numbers provided are in millions of

Q111: A bond is scheduled to mature in

Q112: The following is an FI's balance sheet

Q113: The numbers provided are in millions of

Q115: The following is an FI's balance sheet

Q116: The numbers provided are in millions of

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents