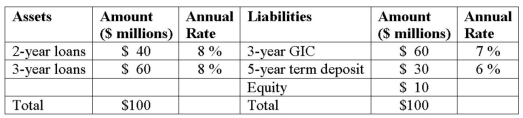

Duration Bank has the following assets and liabilities as of year-end. All assets and liabilities are currently priced at par and pay interest annually.  What is the change in the value of its liabilities if all interest rates decrease by 1 percent?

What is the change in the value of its liabilities if all interest rates decrease by 1 percent?

A) Approximately $2.003 million.

B) Approximately -$2.355 million.

C) Approximately $2.697 million.

D) Approximately $2.906 million.

E) Approximately $3.211 million.

Correct Answer:

Verified

Q99: Hadbucks National Bank current balance sheet appears

Q100: Duration Bank has the following assets and

Q101: Which theory of term structure posits that

Q102: Which theory of term structure argues that

Q103: The liquidity premium theory of the term

Q106: The yield curve

A)relates rates for different maturities

Q107: Duration Bank has the following assets and

Q108: The market segmentation theory of the term

Q108: Which theory of term structure states that

Q109: The unbiased expectations theory of the term

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents