Suppose all firms in an industry have a production technology described by the production function  .The cost of labor is 2 and the cost of capital is 4, and each firm faces a recurring fixed cost of 300.

.The cost of labor is 2 and the cost of capital is 4, and each firm faces a recurring fixed cost of 300.

a.Derive the long run cost and average cost functions for each firm.(Hint: Given the shapes of the isoquants implied by the production function, you should be able to do this without solving a calculus problem.)

b.What is the long run equilibrium output price?

c.How much does each firm produce in long run equilibrium?

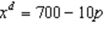

d.Suppose market demand is given by  .How many firms are in the industry in long run equilibrium?

.How many firms are in the industry in long run equilibrium?

e.Suppose the industry is currently in long run equilibrium.Derive the short run cost function for each firm (assuming labor is variable but capital is fixed in the short run).f.Now suppose that demand falls to  .What happens to output price in the short run? What happens to price and the number of firms in the long run?

.What happens to output price in the short run? What happens to price and the number of firms in the long run?

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q14: Suppose there are no recurring fixed costs

Q15: A drop in output demand accompanied by

Q16: Whenever a firm is making positive economic

Q17: An increase in license fees -- a

Q18: The reason long run market supply curves

Q19: If all firms are identical, output demand

Q20: Equilibrium prices coordinate the actions of producers

Q21: Suppose gasoline stations operate with identical costs

Q23: Suppose you are Joe -- one of

Q24: Suppose all firms in a perfectly competitive

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents