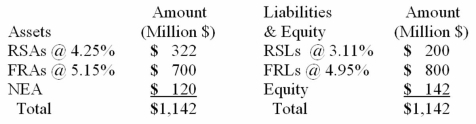

After conducting a rate-sensitive analysis,a bank finds itself with the following amounts of rate-sensitive assets and liabilities (RSAs and RSL) and fixed-rate assets and liabilities (FRAs and FRLs) ; the rate of return and cost rates on the accounts are also given:  If the bank wishes to set up a swap to totally hedge the interest rate risk,the bank should

If the bank wishes to set up a swap to totally hedge the interest rate risk,the bank should

A) pay a variable rate of interest and receive a fixed rate of interest.

B) pay a fixed rate of interest and receive a variable rate of interest.

C) pay a variable rate of interest and receive a variable rate of interest.

D) pay a fixed rate of interest and receive a fixed rate of interest.

Correct Answer:

Verified

Q36: The safest way to hedge a bond

Q37: For a bond put option,the _ the

Q38: A _ position in T-bond futures should

Q39: Basis risk occurs because it is generally

Q40: The safest way to hedge a bond

Q43: A U.S. bank has deposit liabilities denominated

Q45: Is it safer to hedge a contingent

Q57: A U.S. firm is earning British pounds

Q58: In terms of direct costs,are futures or

Q61: A bank wishes to hedge its $25

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents