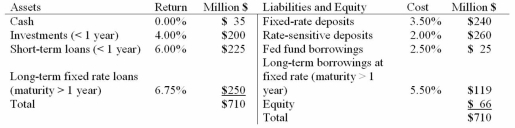

A bank has the following balance sheet:  If the spread effect is zero and all interest rates decline 50 basis points,the bank's NII will change by ________________ over the year.

If the spread effect is zero and all interest rates decline 50 basis points,the bank's NII will change by ________________ over the year.

A) $0

B) $400,000

C) -$400,000

D) $700,000

E) -$700,000

Correct Answer:

Verified

Q19: If DA > kDL,then falling interest rates

Q21: A bank has the following balance sheet:

Q21: A bank has three assets. It has

Q22: For large interest rate declines,duration _ the

Q25: For a nine-month maturity bucket,the bank has

Q26: After interest rate and yield curve changes,a

Q26: A bank has DA = 2.4 years

Q27: A bank has a negative repricing gap

Q29: The structure of a bank's balance sheet

Q29: A bank has a positive duration gap.

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents