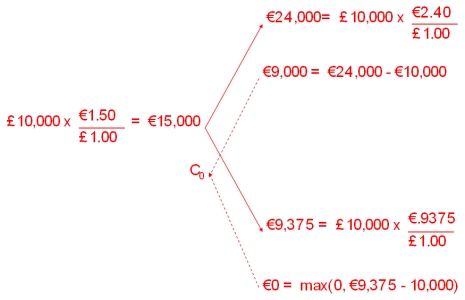

Use the binomial option pricing model to find the value of a call option on £10,000 with a strike price of €12,500. The current exchange rate is €1.50/£1.00 and in the next period the exchange rate can increase to €2.40/£ or decrease to €0.9375/€1.00 .

The current interest rates are i€ = 3% and are i£ = 4%.

Choose the answer closest to yours.

A) €3,275

B) €2,500

C) €3,373

D) €3,243  And thereby the value call is

And thereby the value call is

Correct Answer:

Verified

Q28: Open interest in currency futures contracts

A)tends to

Q39: The current spot exchange rate is $1.55

Q45: Find the value of a call option

Q48: Draw the tree for a put option

Q49: For an American call option,A and B

Q51: Which of the following is correct?

A)Time value

Q51: Which of the following is correct?

A)European options

Q55: For European currency options written on euro

Q55: For European currency options written on euro

Q56: You have written a call option on

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents