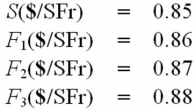

Consider the following spot and forward rate quotations for the Swiss franc:  Calculate the three-month forward premium in American terms.Assume 30-day months and 360-day years.

Calculate the three-month forward premium in American terms.Assume 30-day months and 360-day years.

A) 0.353.

B) 0.4235.

C) 0.1364.

D) 0.1412.

Correct Answer:

Verified

Q78: Which of the following are correct?

A)

Q79: Which of the following is correct?

A)

Q80: For a U.S. trader working in American

Q81: The SF/$ 180-day forward exchange rate is

Q82: Bank dealers in conversations among themselves use

Q86: Consider the balance sheets of Bank A

Q88: The €/$ spot exchange rate is $1.50/€

Q88: Consider the balance sheets of Bank A

Q91: Q93: ![]()

![]()

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents