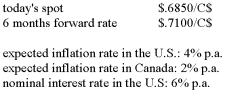

You have the following information:  You are asked to forecast the spot exchange rate between the Canadian dollar and the U.S.dollar in six months.

You are asked to forecast the spot exchange rate between the Canadian dollar and the U.S.dollar in six months.

a)What is your forecast based on purchasing power parity?

b)What is your forecast based on the forward expectations parity?

c)Based on the Fisher effect,what should be the real interest rate in Canada?

d)Why are the two forecasts in a and b different?

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q3: The international Fisher effect is the same

Q13: Deviations from interest rate parity exist for

Q19: Which statement about real exchange rates is

Q20: When Interest Rate Parity (IRP)does not hold

A)there

Q23: Assume the current $/£ exchange rate is

Q25: Suppose that the two-months interest rate is

Q25: The 9-months inflation rate in Great Britain

Q26: Assume the current $/£ exchange rate is

Q28: Suppose that the two-months interest rate is

Q30: The 9-months inflation rate in Great Britain

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents