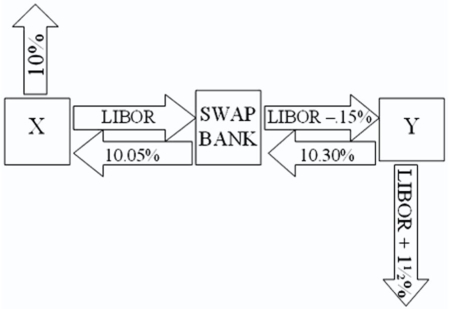

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years.Their external borrowing opportunities are shown here: A swap bank proposes the following interest only swap:

X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR; in exchange the swap bank will pay to company X interest payments on $10,000,000 at a fixed rate of 10.05 percent.Y will pay the swap bank interest payments on $10,000,000 at a fixed rate of 10.30 percent and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of LIBOR ? 0.15 percent.  What is the value of this swap to the swap bank?

What is the value of this swap to the swap bank?

A) The swap bank will earn 40 basis points per year on $10,000,000 = $40,000 per year.

B) The swap bank will earn 10 basis points per year on $10,000,000 = $10,000 per year.

C) The swap bank will lose money.

D) none of the options

Correct Answer:

Verified

Q1: A swap bank has identified two companies

Q2: An interest-only single currency interest rate swap

A)is

Q3: A swap bank

A)can act as a broker,bringing

Q4: Company X wants to borrow $10,000,000

Q6: The size of the swap market (as

Q7: Suppose the quote for a five-year swap

Q8: The term interest rate swap

A)refers to a

Q9: Examples of "single-currency interest rate swap" and

Q10: Company X wants to borrow $10,000,000

Q11: A swap bank makes the following

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents