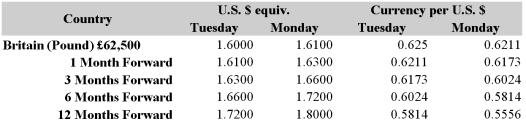

Your firm is a U.S.-based exporter of bicycles. You have sold an order to a French firm for €1,000,000 worth of bicycles. Payment from the French firm (in euro) is due in three months. Detail a strategy using futures contracts that will hedge your exchange rate risk. Have an estimate of how many contracts of what type and how much (in $) your firm will have.

A) Go short 12 six-month forward contracts; pay $1,290,000.

B) Go short 16 six-month forward contracts. Pay $1,230,000.

C) Go long 16 six-month forward contracts; raise $1,230,000.

D) Go long 12 six-month forward contracts. Receive $1,230,000.

Correct Answer:

Verified

Q30: Your firm is a Swiss importer of

Q31: Your firm is a U.K.-based importer of

Q32: Your firm is a U.K.-based exporter of

Q33: Your firm is a Swiss importer of

Q34: Your firm is an Italian exporter of

Q36: Your firm is a U.K.-based exporter of

Q37: Your firm is a Swiss exporter of

Q38: Your firm is a U.K.-based importer of

Q39: Your firm is an Italian exporter of

Q40: Your firm is a Swiss exporter of

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents