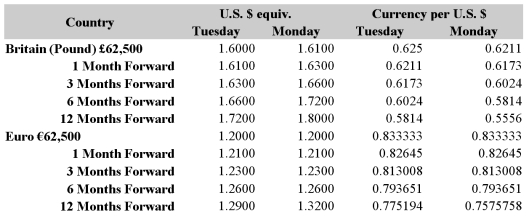

Your firm is a U.K.-based exporter of British bicycles. You have sold an order to an Italian firm for €1,000,000 worth of bicycles. Payment from the Italian firm (in €) is due in twelve months. Your firm wants to hedge the receivable into . Not dollars. Interest rates are 3% in €, 2% in $ and 4% in £.  Detail a strategy using spot exchange rates and borrowing or lending that will hedge your exchange rate risk.

Detail a strategy using spot exchange rates and borrowing or lending that will hedge your exchange rate risk.

A) Borrow €970,873.79 in one year you owe €1m, which will be financed with the receivable. Convert €970,873.79 to dollars at spot, receive $1,165,048.54. Convert dollars to pounds at spot, receive £728,155.34.

B) Sell €1m forward using 16 contracts at $1.20 per €1. Buy £750,000 forward using 12 contracts at $1.60 per £1.

C) Sell €1m forward using 16 contracts at the forward rate of $1.29 per €1. Buy £750,000 forward using 12 contracts at the forward rate of $1.72 per £1.

D) None of the above

Correct Answer:

Verified

Q40: Your firm is a Swiss exporter of

Q41: A Japanese IMPORTER has a €1,000,000 PAYABLE

Q42: A Japanese EXPORTER has a €1,000,000 receivable

Q43: Buying a currency option provides

A)a flexible hedge

Q44: A Japanese IMPORTER has a $1,250,000 PAYABLE

Q46: A Japanese EXPORTER has a €1,000,000 receivable

Q47: From the perspective of a corporate CFO,

Q48: A U.S. firm has sold an Italian

Q50: Your firm is a Swiss exporter of

Q52: XYZ Corporation,located in the United States,has an

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents