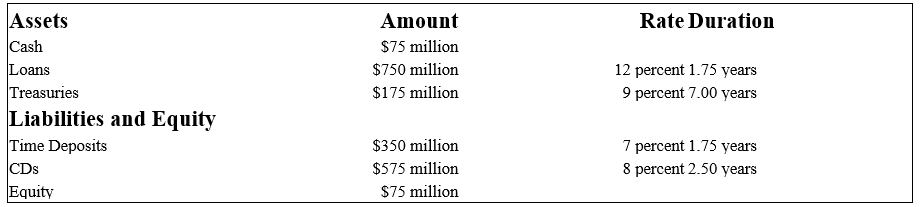

-Calculate the leverage-adjusted duration gap to four decimal places and state the FI's interest rate risk exposure of this institution.

A) +1.0308 years;exposed to interest rate increases.

B) -0.3232 years;exposed to interest rate increases.

C) +0.8666 years;exposed to interest rate increases.

D) +0.4875 years;exposed to interest rate increases.

Correct Answer:

Verified

Q104: A bond is scheduled to mature in

Q114: Q115: The numbers provided are in millions of Q116: U.S. Treasury quotes from the WSJ on Q117: The numbers provided by Fourth Bank of Q118: The numbers provided are in millions of Q121: The following is an FI's balance sheet Q122: The following is an FI's balance sheet Q123: What is the effect of a 100 Q124: The following is an FI's balance sheet![]()

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents