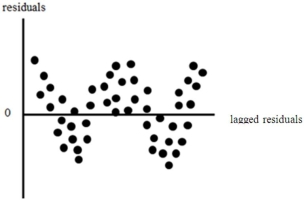

Suppose that you plot the residuals from a regression of GDP on the unemployment rate and you get the following

You would conclude that the error terms are

A) definitely autocorrelated.

B) likely not autocorrelated.

C) possibly autocorrelated and you would perform a formal test for autocorrelation.

D) possibly autocorrelated and you would perform a correction for heteroskedasticity.

Correct Answer:

Verified

Q12: An AR(2)process is written as

A)

Q13: The first step of the Durbin-Watson test

Q14: An AR(1,6)process is written as

A)

Q15: An AR(1)process is written as

A)

Q16: If autocorrelation is not present,then the Durbin-Watson

Q18: If positive autocorrelation is not present,then the

Q19: The third step of the Regression

Q20: The first step of the Regression test

Q21: The final step of the Regression test

Q22: In order to perform cointegration,you need to

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents