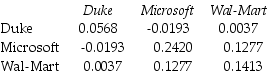

Use the table for the question(s) below.

Consider the following covariances between securities:

-Which of the following formulas is INCORRECT?

A) Variance of an equally Weighted Portfolio = (1 -

) (Average Variance of Individual Stocks) +

(Average covariance between the stocks)

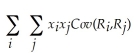

B) Variance of a portfolio =

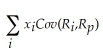

C) Variance of a portfolio =

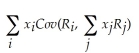

D) Variance of a portfolio =

Correct Answer:

Verified

Q21: Use the table for the question(s)below.

Consider the

Q22: Use the table for the question(s)below.

Consider the

Q24: Consider an equally weighted portfolio that contains

Q25: Use the table for the question(s)below.

Consider the

Q26: Use the table for the question(s)below.

Consider the

Q28: Which of the following statements is FALSE?

A)The

Q29: Use the table for the question(s)below.

Consider the

Q31: Which of the following statements is FALSE?

A)The

Q39: Use the table for the question(s)below.

Consider the

Q40: Which of the following statements is FALSE?

A)The

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents