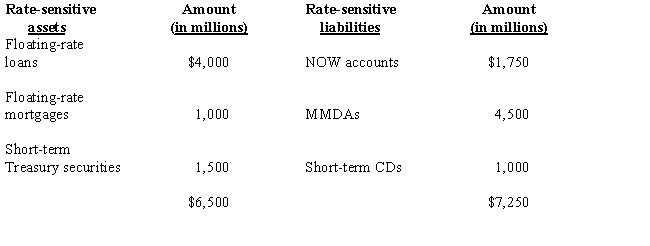

A bank has the following asset and liability portfolios. What is the gap?

A) $750 million

B) -$750 million

C) 1.12

D) .896

E) none of the above

Correct Answer:

Verified

Q7: As the secondary market for loans has

Q10: The _ of interest rate futures _

Q19: When cash outflows temporarily exceed cash inflows,

Q20: Petri Bank had interest revenues of $70

Q21: Banks generally _ loans and _ their

Q21: Which of the following loan portfolios are

Q24: Banks would reduce their liquidity position by

Q25: Banks can reduce their default risk by

Q27: A bank has the following asset and

Q28: Banks can increase their liquidity position by

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents