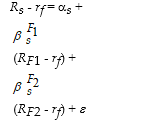

Use the equation for the question(s) below.

Consider the following regression model:

-The term  is a(n)

is a(n)

A) measure of the expected percent change in the excess return of a security for a 1% change in the excess return of the second factor portfolio.

B) error term that has an expectation of zero and is uncorrelated with either factor.

C) constant term.

D) measure of the expected percent change in the excess return of a security for a 1% change in the excess return of the first factor portfolio.

Correct Answer:

Verified

Q44: Use the information for the question(s) below.

Consider

Q48: Use the information for the question(s)below.

Consider two

Q49: The size effect reflects the fact that

Q51: The size effect reveals that stocks with

Q52: Book-to-market ratio is the ratio of _.

A)

Q53: Which of the following statements is false?

A)

Q53: All else being equal a _ alpha

Q56: One of the reasons that it is

Q58: Use the figure for the question(s)below.Consider the

Q60: A group of portfolios from which we

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents