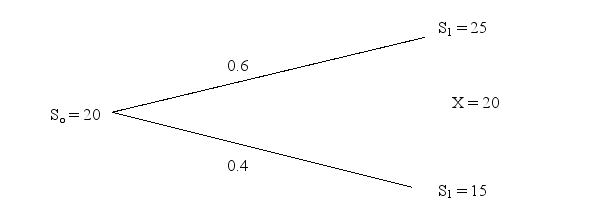

Francis is long the underlying and has sold h number of call options with the following binomial tree:

Given the current asset price is $20 and r is 5%,what is the price of the above call option?

A) $2.86

B) $0.60

C) $21.43

D) −$21.43

Correct Answer:

Verified

Q29: Which of the following best defines implied

Q45: Create a table illustrating the range of

Q46: Suppose Jo's stock price is currently $100.In

Q47: Toronto Skaters' stock is now worth $100.In

Q49: (Assume: continuous compounding and value of the

Q49: Briefly explain how to replicate the payoff

Q50: _is an estimate of the _ of

Q51: VIX can be used

A)to price interest rate

Q52: The current stock price is $568.36,a one-year

Q54: Create a table depicting the payoffs for

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents