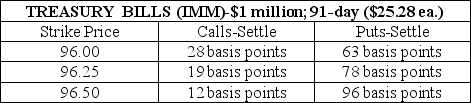

23-81 A bank with total assets of $271 million and equity of $31 million has a leverage adjusted duration gap of +0.21 years.Use the following quotation from the Wall Street Journal to construct an at-the-money futures option hedge of the bank's duration gap position.  If 91-day Treasury bill rates increase from 3.75 percent to 4.75 percent,what will be the profit/loss per contract on the bank's futures option hedge?

If 91-day Treasury bill rates increase from 3.75 percent to 4.75 percent,what will be the profit/loss per contract on the bank's futures option hedge?

A) A loss of $556.16 per put option contract.

B) A profit of $556.16 per put option contract.

C) A loss of $1,971.84 per call option contract.

D) A profit of $1,971.84 per call option contract.

E) A profit of $2,528 per put option contract.

Correct Answer:

Verified

Q82: 23-87 Given the expected one-year rates in

Q83: 23-88 If the manager buys a one-year

Q84: 23-85 Buying a cap option agreement

A)means buying

Q85: 23-90 What is the yield to maturity

Q86: 23-86 What is the yield to maturity

Q88: 23-91 Given the expected one-year rates in

Q89: 23-94 The duration of the T-notes,Baa bonds,and

Q90: 23-99 At the time of placement,the premium

Q91: 23-84 A digital default option

A)always pays the

Q92: 23-97 On the advice of its chief

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents