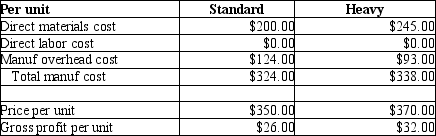

AAA Metal Bearings produces two sizes of metal bearings (sold by the crate)-standard and heavy. The standard bearings require $200 of direct materials per unit (per crate)and the heavy bearings require $245 of direct materials per unit. The operation is mechanized and there is no direct labor. Previously AAA used a single plantwide allocation rate for manufacturing overhead, which was $1.55 per machine hour. Based on the single rate, gross profit data were as follows:

Although the data showed that the heavy bearings were more profitable than the standard bearings, the plant manager knew that the heavy bearings required much more processing in the metal fabrication phase than the standard bearings, and that this factor was not adequately reflected in the single allocation rate. He suspected that it was distorting the profit data. He suggested adopting an activity-based costing approach.

Although the data showed that the heavy bearings were more profitable than the standard bearings, the plant manager knew that the heavy bearings required much more processing in the metal fabrication phase than the standard bearings, and that this factor was not adequately reflected in the single allocation rate. He suspected that it was distorting the profit data. He suggested adopting an activity-based costing approach.

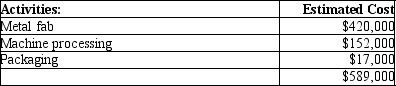

Working together, the engineers and accountants identified the following three manufacturing activities, and broke down the annual overhead costs as shown:

Engineers believed that metal fabrication costs should be allocated by weight, and estimated that the plant processed 12,000 kilos of metal per year. Machine processing costs were correlated to machine hours, and the engineers estimated a total of 380,000 machine hours for the year. Packaging costs were the same for both types of products, and so they could be allocated simply by the number of units produced. The production plan provided for 4,000 units of standard and 1,000 units of heavy bearings to be produced during the year. Additional data on a per unit basis are as follows:

Engineers believed that metal fabrication costs should be allocated by weight, and estimated that the plant processed 12,000 kilos of metal per year. Machine processing costs were correlated to machine hours, and the engineers estimated a total of 380,000 machine hours for the year. Packaging costs were the same for both types of products, and so they could be allocated simply by the number of units produced. The production plan provided for 4,000 units of standard and 1,000 units of heavy bearings to be produced during the year. Additional data on a per unit basis are as follows:

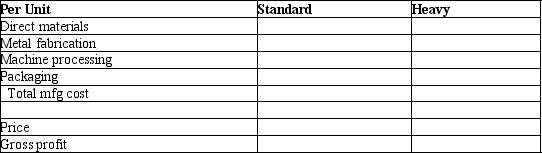

Using the data above, please calculate activity rates. Then, following the ABC methodology, calculate the production cost and gross profit for both product types, using the format below:

Using the data above, please calculate activity rates. Then, following the ABC methodology, calculate the production cost and gross profit for both product types, using the format below:

Correct Answer:

Verified

Q22: Which of the following would most likely

Q41: An activity-based costing system improves the allocation

Q49: Ace Plastics produces many different kinds of

Q50: AAA Metal Bearings produces two sizes of

Q52: Formosa Steel Products makes steel building materials

Q54: Orlando Avionics makes three types of radios

Q55: Target cost is the price that customers

Q55: Orlando Avionics makes three types of radios

Q57: Orlando Avionics makes three types of radios

Q58: Ace Plastics produces many different kinds of

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents