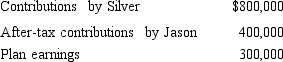

At the time of his death, Jason was a participant in Silver Corporation's qualified pension plan and group term life insurance. The balance of the survivorship feature in his pension plan is:  The term insurance has a maturity value of $100,000. All amounts are paid to Pam, Jason's daughter. One result of these transactions is:

The term insurance has a maturity value of $100,000. All amounts are paid to Pam, Jason's daughter. One result of these transactions is:

A) Pam must pay income tax on $300,000.

B) Pam must pay income tax on $1,100,000.

C) Jason's gross estate must include $1,200,000.

D) Jason's gross estate must include $1,500,000.

E) None of the above.

Correct Answer:

Verified

Q81: Which, if any, of the following items

Q83: Concerning the formula for the Federal estate

Q96: Which of the following is not a

Q101: Mark dies on March 6, 2013. Which,

Q102: Prior to her death in 2013, Alma

Q105: Which of the following statements relating to

Q106: At the time of his death, Lance

Q107: Matt and Patricia are husband and wife

Q108: In 2005, Mandy and Hal (mother and

Q119: Which, if any, of the following is

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents