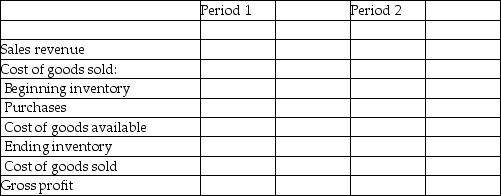

Football, Inc.'s clerk made a mistake while preparing the financial statements. The ending inventory for Year 1 should have been $20,000, but the clerk recorded it as $23,000 on the income statement. Assume that sales for Years 1 and 2 are $90,000 per year and purchases are $20,000 per year. Beginning inventory for Year 1 of $12,000 and ending inventory for Year 2 of $21,000 were correctly recorded. Complete the following income statement for Year 1 and 2.

Correct Answer:

Verified

Q9: Under the periodic inventory system, a physical

Q133: Beginning inventory and ending inventory have opposite

Q136: If ending inventory is understated for Year

Q165: Make Money Company Inc. had beginning inventory

Q167: If ending inventory for the period is

Q169: There is an error in computing ending

Q170: Ending inventory for the year ended December

Q171: Crazy Eddie "cooked the books" which ultimately

Q172: In the periodic inventory system, the inventory

Q173: Happy House Corporation reported net sales of

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents