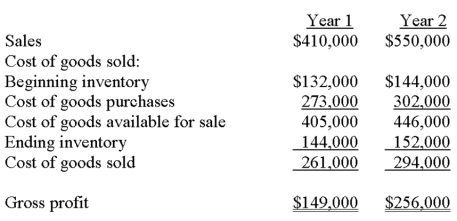

Louise Company reported the following income statement information for Year 1 and Year 2:  The beginning inventory balance for Year 1 is correct. The ending inventory balance for Year 2 is also correct. However, the ending inventory figure for Year 1 was overstated by $20,000. Given this information, the correct gross profit figures for Year 1 and Year 2 would be:

The beginning inventory balance for Year 1 is correct. The ending inventory balance for Year 2 is also correct. However, the ending inventory figure for Year 1 was overstated by $20,000. Given this information, the correct gross profit figures for Year 1 and Year 2 would be:

A) $129,000 for Year 1 and $256,000 for Year 2.

B) $281,000 for Year 1 and $274,000 for Year 2.

C) $129,000 for Year 1 and $276,000 for Year 2.

D) $169,000 for Year 1 and $236,000 for Year 2.

E) $169,000 for Year 1 and $276,000 for Year 2.

Correct Answer:

Verified

Q82: The inventory valuation method that identifies each

Q84: Axme Corporation uses a weighted-average perpetual inventory

Q85: A company had inventory on November 1

Q87: Tops had cost of goods sold of

Q91: A company had the following purchases during

Q93: Given the following information, determine the cost

Q93: Days' sales in inventory:

A) Is also called

Q94: The inventory turnover ratio:

A) Is used to

Q95: A company has inventory of 15 units

Q100: Axme uses a weighted average perpetual inventory

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents