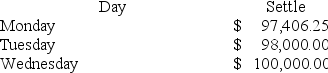

On Monday morning you sell one June T-bond futures contract at $97,843.75. The contract's face value is $100,000. The initial margin requirement is $2,700, and the maintenance margin requirement is $2,000 per contract. Use the following price data to answer the following questions.

The cumulative rate of return on your investment after Wednesday is a ________.

A) 79.9% loss

B) 2.6% loss

C) 33% gain

D) 53.9% loss

Correct Answer:

Verified

Q70: You believe that the spread between the

Q71: On Monday morning you sell one June

Q72: The _ contract dominates trading in stock-index

Q73: If the risk-free rate is greater than

Q74: A 1-year gold futures contract is selling

Q76: From the perspective of determining profit and

Q77: The _ and the _ have the

Q78: You own a $15 million bond portfolio

Q79: A hypothetical futures contract on a nondividend-paying

Q80: You purchase an interest rate futures contract

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents