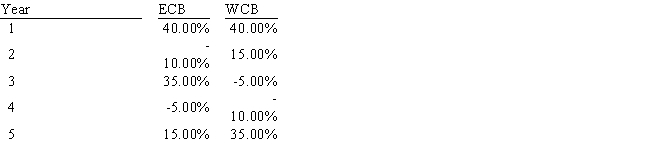

Assume that your uncle holds just one stock,East Coast Bank (ECB) ,which he thinks has very little risk.You agree that the stock is relatively safe,but you want to demonstrate that his risk would be even lower if he were more diversified.You obtain the following returns data for West Coast Bank (WCB) .Both banks have had less variability than most other stocks over the past 5 years.Measured by the standard deviation of returns,by how much would your uncle's risk have been reduced if he had held a portfolio consisting of 54% in ECB and the remainder in WCB? (Hint: Use the sample standard deviation formula. ) Do not round your intermediate calculations.

A) 3.59%

B) 4.27%

C) 2.99%

D) 3.99%

E) 4.51%

Correct Answer:

Verified

Q124: Porter Inc's stock has an expected return

Q127: Mulherin's stock has a beta of 1.23,its

Q137: Company A has a beta of 0.70,while

Q139: Roenfeld Corp believes the following probability distribution

Q141: Assume that you manage a $10.00 million

Q141: Returns for the Dayton Company over the

Q142: Assume that you are the portfolio manager

Q143: A mutual fund manager has a $40

Q144: Carson Inc.'s manager believes that economic conditions

Q146: CCC Corp has a beta of 1.5

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents