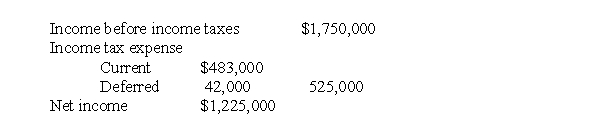

Columbia Corp.'s partial income statement for its first year of operations is as follows:  Columbia uses straight-line depreciation for financial reporting purposes and CCA for tax purposes. The depreciation expense for the year was $700,000. Except for depreciation, there were no other differences between accounting income and taxable income. Assuming a 30% tax rate, what amount was claimed for CCA on the corporation's tax return for the year?

Columbia uses straight-line depreciation for financial reporting purposes and CCA for tax purposes. The depreciation expense for the year was $700,000. Except for depreciation, there were no other differences between accounting income and taxable income. Assuming a 30% tax rate, what amount was claimed for CCA on the corporation's tax return for the year?

A) $560,000

B) $665,000

C) $700,000

D) $840,000

Correct Answer:

Verified

Q22: Taxable income of a corporation

A) differs from

Q25: Casey Inc. uses the accrual method of

Q26: For calendar 2017, Melvin Corp. reported depreciation

Q27: For calendar 2017, Peanuts Corp. prepared the

Q28: Tax rates other than the current tax

Q31: On January 1, 2017, Wings Inc. purchased

Q32: Using IFRS, IAS 12 guidelines allow for

Q33: For calendar 2017, its first year of

Q34: For calendar 2017, its first year of

Q41: Allocating income tax expense or benefit for

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents