Deck 16: Management Control Systems

Full screen (f)

Question

Question

Figure 16-1

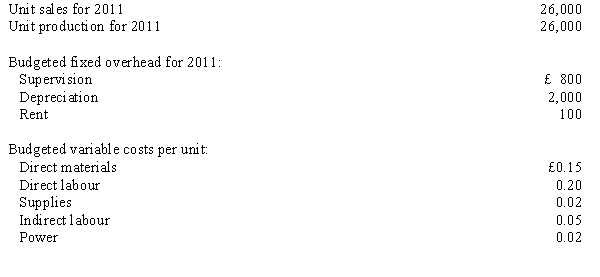

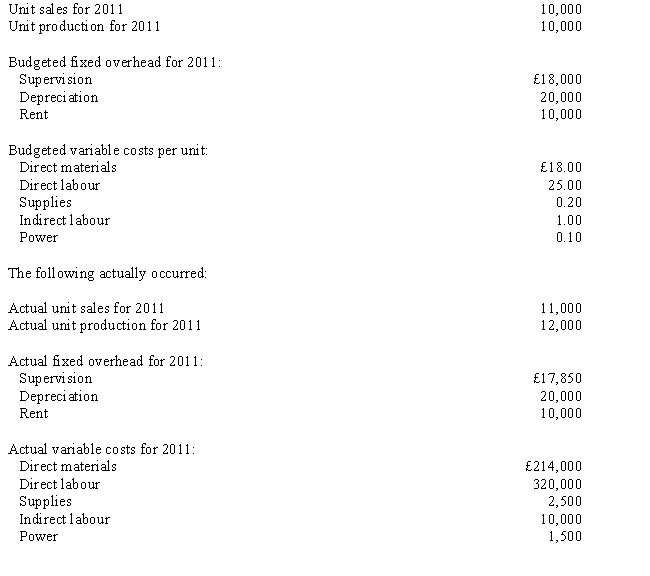

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

The following actually occurred:

Refer to Figure 16-1. The flexible budget variance for indirect labour for 2011 is

A) £1,250 F.

B) £50 F.

C) £50 U.

D) £1,200 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget variance for indirect labour for 2011 is

A) £1,250 F.

B) £50 F.

C) £50 U.

D) £1,200 U.

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget variance for supplies is

A) £10 U.

B) £10 F.

C) £50 U.

D) £50 F.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget variance for supplies is

A) £10 U.

B) £10 F.

C) £50 U.

D) £50 F.

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget variance for direct materials is

A) £100 F.

B) £100 U.

C) £400 F.

D) £400 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget variance for direct materials is

A) £100 F.

B) £100 U.

C) £400 F.

D) £400 U.

Question

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The flexible budget for direct materials cost in 2011 is

A) £3,500.

B) £3,600.

C) £3,900.

D) £4,000.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget for direct materials cost in 2011 is

A) £3,500.

B) £3,600.

C) £3,900.

D) £4,000.

Question

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The flexible budget for rent in 2011 is

A) £100.

B) £200.

C) £2,900.

D) £2,950.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget for rent in 2011 is

A) £100.

B) £200.

C) £2,900.

D) £2,950.

Question

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The flexible budget variance for total cost for 2011 is

A) £90 U.

B) £140 U.

C) £230 U.

D) £50 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget variance for total cost for 2011 is

A) £90 U.

B) £140 U.

C) £230 U.

D) £50 U.

Question

Question

Question

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget variance for total fixed overhead is

A) £50 U.

B) £50 F.

C) £-0-.

D) £100 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget variance for total fixed overhead is

A) £50 U.

B) £50 F.

C) £-0-.

D) £100 U.

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The total flexible budgeted costs for 2011 are

A) £10,560.

B) £13,460.

C) £13,510.

D) £11,340.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The total flexible budgeted costs for 2011 are

A) £10,560.

B) £13,460.

C) £13,510.

D) £11,340.

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget for total variable costs is

A) £90 U.

B) £180 U.

C) £790 F.

D) £880 F.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget for total variable costs is

A) £90 U.

B) £180 U.

C) £790 F.

D) £880 F.

Question

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget variance for rent is

A) £100 F.

B) £100 U.

C) £-0-.

D) £50 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget variance for rent is

A) £100 F.

B) £100 U.

C) £-0-.

D) £50 U.

Question

Question

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The flexible budget variance for supervision for 2011 is

A) £67 F.

B) £67 U.

C) £50 F.

D) none of these.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget variance for supervision for 2011 is

A) £67 F.

B) £67 U.

C) £50 F.

D) none of these.

Question

Figure 16-2

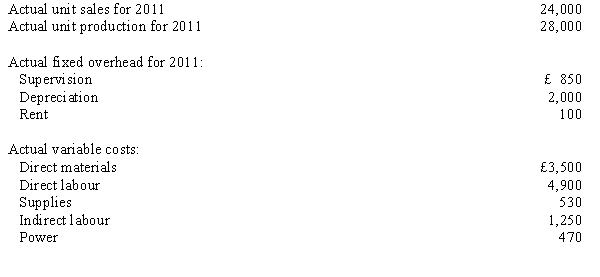

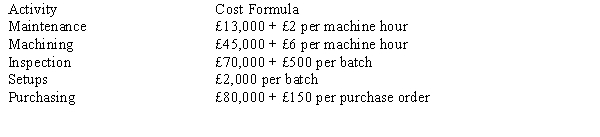

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for purchasing in an activity-based performance report?

A) £1,000 U

B) £2,000 U

C) £3,000 U

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for purchasing in an activity-based performance report?

A) £1,000 U

B) £2,000 U

C) £3,000 U

D) none of the above

Question

Figure 16-4

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed: Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders

Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders  The following variances were given in the activity performance report:

The following variances were given in the activity performance report:

Refer to Figure 16-4. What is the activity variance for design?

A) £40 F

B) £30 U

C) £15 F

D) £100 U

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed:

Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report: Refer to Figure 16-4. What is the activity variance for design?

A) £40 F

B) £30 U

C) £15 F

D) £100 U

Question

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for inspection in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for inspection in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Question

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for maintenance in an activity-based performance report?

A) £50 F

B) £50 U

C) £550 U

D) £550 F

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for maintenance in an activity-based performance report?

A) £50 F

B) £50 U

C) £550 U

D) £550 F

Question

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for maintenance in an activity-based performance report?

A) £1,000 U

B) £3,000 U

C) £3,000 F

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for maintenance in an activity-based performance report?

A) £1,000 U

B) £3,000 U

C) £3,000 F

D) none of the above

Question

Question

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for machining in an activity-based performance report?

A) £1,000 U

B) £2,000 U

C) £3,000 U

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for machining in an activity-based performance report?

A) £1,000 U

B) £2,000 U

C) £3,000 U

D) none of the above

Question

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for machining in an activity-based performance report?

A) £50 F

B) £50 U

C) £800 U

D) none of the above

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for machining in an activity-based performance report?

A) £50 F

B) £50 U

C) £800 U

D) none of the above

Question

Figure 16-4

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed: Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report:

Refer to Figure 16-4. What is the actual cost of machining?

A) £24,970

B) £25,010

C) £25,050

D) none of the above

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed:

Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report: Refer to Figure 16-4. What is the actual cost of machining?

A) £24,970

B) £25,010

C) £25,050

D) none of the above

Question

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for total costs in an activity-based performance report?

A) £700 U

B) £700 F

C) £800 U

D) none of the above

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for total costs in an activity-based performance report?

A) £700 U

B) £700 F

C) £800 U

D) none of the above

Question

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for setups in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for setups in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Question

Question

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for purchasing in an activity-based performance report?

A) £50 F

B) £50 U

C) £100 U

D) none of the above

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for purchasing in an activity-based performance report?

A) £50 F

B) £50 U

C) £100 U

D) none of the above

Question

Figure 16-4

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed: Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report:

Refer to Figure 16-4. What is the activity variance for purchasing?

A) £500 U

B) £100 U

C) £50 U

D) none of the above

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed:

Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report: Refer to Figure 16-4. What is the activity variance for purchasing?

A) £500 U

B) £100 U

C) £50 U

D) none of the above

Question

Figure 16-4

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed: Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report:

Refer to Figure 16-4. What is the actual cost of setups?

A) £160

B) £190

C) £300

D) none of the above

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed:

Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report: Refer to Figure 16-4. What is the actual cost of setups?

A) £160

B) £190

C) £300

D) none of the above

Question

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for total costs in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for total costs in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Question

Question

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for setups in an activity-based performance report?

A) £50 F

B) £50 U

C) £800 U

D) none of the above

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for setups in an activity-based performance report?

A) £50 F

B) £50 U

C) £800 U

D) none of the above

Question

Question

Question

Glock, SA., is looking for feedback on performance. The company compares the budget for the year with the actual costs.

Glock had the following budgeted data: Required:

Required:

Prepare a flexible budget for production costs for the following range of activity: 2,500 units; 4,000 units; 6,000 units.

Glock had the following budgeted data:

Required:Prepare a flexible budget for production costs for the following range of activity: 2,500 units; 4,000 units; 6,000 units.

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. Which of the following describes the flexible budget variance for March?

A) The fixed overhead variance is £100 F.

B) The variable overhead variance is £1,000 U.

C) The variable overhead variance is £1,100 F.

D) both a and c

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. Which of the following describes the flexible budget variance for March?

A) The fixed overhead variance is £100 F.

B) The variable overhead variance is £1,000 U.

C) The variable overhead variance is £1,100 F.

D) both a and c

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which of the following departments would NOT be classified as a profit centre?

A) the accounting department of a large PLc

B) the automotive division of a large PLc

C) the hardware department of a department store

D) the men's shoe department of a department store

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which of the following departments would NOT be classified as a profit centre?

A) the accounting department of a large PLc

B) the automotive division of a large PLc

C) the hardware department of a department store

D) the men's shoe department of a department store

Question

Question

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Before implementing a responsibility accounting system, all areas of authority and responsibility within an organization must be clearly defined. Explain how this accomplished and why it is important.

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Before implementing a responsibility accounting system, all areas of authority and responsibility within an organization must be clearly defined. Explain how this accomplished and why it is important.

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which of the following facets of a responsibility accounting system is most likely to lead employees to distrust the entire budgeting and performance evaluation system?

A) tight standards

B) well-defined standards

C) budget participation

D) static qualifiers

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which of the following facets of a responsibility accounting system is most likely to lead employees to distrust the entire budgeting and performance evaluation system?

A) tight standards

B) well-defined standards

C) budget participation

D) static qualifiers

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Klamaty, SA., is looking for feedback on performance. The company compares the budget for the year with the actual costs.

Klamaty, SA., had the following budgeted data: Required:

Required:

a.

Prepare a performance report for all costs showing static budget variances.

b.

Prepare a performance report for all costs showing flexible budget variances.

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Klamaty, SA., is looking for feedback on performance. The company compares the budget for the year with the actual costs.

Klamaty, SA., had the following budgeted data:

Required: a.

Prepare a performance report for all costs showing static budget variances.

b.

Prepare a performance report for all costs showing flexible budget variances.

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. Which of the following describes how well the plant manager performed for the month of March?

A) The manager performed a good job in controlling costs.

B) The manager performed a poor job in controlling costs.

C) The manager exceeded his goals.

D) both a and c

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. Which of the following describes how well the plant manager performed for the month of March?

A) The manager performed a good job in controlling costs.

B) The manager performed a poor job in controlling costs.

C) The manager exceeded his goals.

D) both a and c

Question

Mertz, SA., has done a cost analysis for its production of flags. The following activities and cost drivers have been developed:  Following are the actual costs of producing 75,000 flags:

Following are the actual costs of producing 75,000 flags:

1,000 machine hours; 15 batches; 10 purchase orders Required:

Required:

Prepare an activity-based performance report.

Following are the actual costs of producing 75,000 flags:1,000 machine hours; 15 batches; 10 purchase orders

Required:Prepare an activity-based performance report.

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. What is the flexible budget for March?

A) £28,800

B) £29,800

C) £30,900

D) £31,680

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. What is the flexible budget for March?

A) £28,800

B) £29,800

C) £30,900

D) £31,680

Question

Question

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

A manager of a profit centre:

A) does not control revenues.

B) does not control expenses.

C) does not control investments.

D) only controls revenues.

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

A manager of a profit centre:

A) does not control revenues.

B) does not control expenses.

C) does not control investments.

D) only controls revenues.

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

What results could be expected by placing pressure on management to perform at certain levels?

A) Lower level managers could become frustrated if they believe upper management is placing a burden on them for costs out of their control.

B) Managers may resort to unethical practices to compensate for unfavorable results.

C) Efforts to deal with immediate controllable factors could become diluted.

D) All the responses could be correct.

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

What results could be expected by placing pressure on management to perform at certain levels?

A) Lower level managers could become frustrated if they believe upper management is placing a burden on them for costs out of their control.

B) Managers may resort to unethical practices to compensate for unfavorable results.

C) Efforts to deal with immediate controllable factors could become diluted.

D) All the responses could be correct.

Question

Riemay, SA., has done a cost analysis for its production of sports cards. The following activities and cost drivers have been developed:  Following are the actual costs of producing 35,000 cards:

Following are the actual costs of producing 35,000 cards:

60 labour hours; 500 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report:

The following variances were given in the activity performance report:  Required:

Required:

Find the missing values.

Prepare an activity-based performance report in good form

Following are the actual costs of producing 35,000 cards:60 labour hours; 500 machine hours; 5 batches; 30 purchase orders

The following variances were given in the activity performance report: Required:Find the missing values.

Prepare an activity-based performance report in good form

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which cost centre listed below is evaluated with the aid of flexible budgets drawn up for the actual level of activity?

A) discretionary cost centres

B) standard cost centres

C) non-relational cost centres

D) flexible cost centres

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which cost centre listed below is evaluated with the aid of flexible budgets drawn up for the actual level of activity?

A) discretionary cost centres

B) standard cost centres

C) non-relational cost centres

D) flexible cost centres

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. What is the flexible budget variance for March?

A) £-0-

B) £1,200 F

C) £900 U

D) £1,100 F

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. What is the flexible budget variance for March?

A) £-0-

B) £1,200 F

C) £900 U

D) £1,100 F

Question

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which of the following departments is likely to be evaluated as a discretionary cost centre?

A) the machining department of an automotive division

B) the food products division of a large PLc

C) the personnel department of an automotive division

D) the Men's shoe department of a department store

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which of the following departments is likely to be evaluated as a discretionary cost centre?

A) the machining department of an automotive division

B) the food products division of a large PLc

C) the personnel department of an automotive division

D) the Men's shoe department of a department store

Question

Question

Timothy, SA., uses a flexible budget for overhead costs. The company expects to produce 40,000 units of the product it manufactures. Each unit requires 0.40 direct labour hours. The cost formulas for each of the four overhead items (where X is measured in direct labour hours) is as follows:  Required:

Required:

a.

Prepare an overhead budget for the expected activity level for the coming year.

b.

Prepare an overhead budget that reflects production that is 25 per cent lower than expected.

Required: a.

Prepare an overhead budget for the expected activity level for the coming year.

b.

Prepare an overhead budget that reflects production that is 25 per cent lower than expected.

Question

Classics, SA., uses a flexible budget for overhead costs. The company expects to produce 20,000 units of the product it manufactures. Half of the units require 0.50 direct labour hours per unit. The remainder requires 0.75 direct labour hours per unit. The cost formulas for each of the four overhead items is as follows:  Required:

Required:

a.

Prepare an overhead budget for the expected activity level for the coming year.

b.

Prepare an overhead budget that reflects production that is 10 per cent higher than expected.

Required: a.

Prepare an overhead budget for the expected activity level for the coming year.

b.

Prepare an overhead budget that reflects production that is 10 per cent higher than expected.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/64

Play

Full screen (f)

Deck 16: Management Control Systems

1

The static budget variance for materials is £200 F and the budgeted cost for materials is £52,000. If the budgeted volume is 13,000 and the actual volume is 13,500, then the flexible budget variance is

A) £2,200 F.

B) £3,000 F.

C) £2,000 F.

D) £1,800 F.

A) £2,200 F.

B) £3,000 F.

C) £2,000 F.

D) £1,800 F.

A

2

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The flexible budget variance for indirect labour for 2011 is

A) £1,250 F.

B) £50 F.

C) £50 U.

D) £1,200 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget variance for indirect labour for 2011 is

A) £1,250 F.

B) £50 F.

C) £50 U.

D) £1,200 U.

C

3

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget variance for supplies is

A) £10 U.

B) £10 F.

C) £50 U.

D) £50 F.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget variance for supplies is

A) £10 U.

B) £10 F.

C) £50 U.

D) £50 F.

A

4

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget variance for direct materials is

A) £100 F.

B) £100 U.

C) £400 F.

D) £400 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget variance for direct materials is

A) £100 F.

B) £100 U.

C) £400 F.

D) £400 U.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is not an objective of responsibility accounting?

A) to redesign processes to be more effective

B) to align individual and organizational goals

C) to influence behaviour

D) to increase profitability

A) to redesign processes to be more effective

B) to align individual and organizational goals

C) to influence behaviour

D) to increase profitability

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

6

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The flexible budget for direct materials cost in 2011 is

A) £3,500.

B) £3,600.

C) £3,900.

D) £4,000.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget for direct materials cost in 2011 is

A) £3,500.

B) £3,600.

C) £3,900.

D) £4,000.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

7

If the static budget variance for materials is £200 F and the budgeted cost for materials is £52,000, then the actual cost of materials is

A) £52,000.

B) £52,200.

C) £51,200.

D) £51,800.

A) £52,000.

B) £52,200.

C) £51,200.

D) £51,800.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

8

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The flexible budget for rent in 2011 is

A) £100.

B) £200.

C) £2,900.

D) £2,950.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget for rent in 2011 is

A) £100.

B) £200.

C) £2,900.

D) £2,950.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

9

The budget most appropriate for control purposes is the

A) static budget.

B) flexible budget.

C) continuous budget.

D) incremental budget.

A) static budget.

B) flexible budget.

C) continuous budget.

D) incremental budget.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

10

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The flexible budget variance for total cost for 2011 is

A) £90 U.

B) £140 U.

C) £230 U.

D) £50 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget variance for total cost for 2011 is

A) £90 U.

B) £140 U.

C) £230 U.

D) £50 U.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

11

When budgets are used for control,

A) budgeted amounts from different years are compared.

B) actual amounts from different years are compared.

C) budgeted amounts are compared to actual amounts.

D) None of these is correct.

A) budgeted amounts from different years are compared.

B) actual amounts from different years are compared.

C) budgeted amounts are compared to actual amounts.

D) None of these is correct.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

12

If production was budgeted at 400 units and the actual production was 420 units, what would be the static budget variance for materials if the actual cost of materials was £4,150 and the budgeted cost per unit is £10?

A) £50 F

B) £200 U

C) £100 F

D) £150 U

A) £50 F

B) £200 U

C) £100 F

D) £150 U

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

13

If production was budgeted at 400 units and the actual production was 420 units, what would be the flexible budget variance for materials if the actual cost of materials was £4,150 and the budgeted cost per unit is £10?

A) £50 F

B) £200 U

C) £100 F

D) £150 U

A) £50 F

B) £200 U

C) £100 F

D) £150 U

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

14

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget variance for total fixed overhead is

A) £50 U.

B) £50 F.

C) £-0-.

D) £100 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget variance for total fixed overhead is

A) £50 U.

B) £50 F.

C) £-0-.

D) £100 U.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

15

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The total flexible budgeted costs for 2011 are

A) £10,560.

B) £13,460.

C) £13,510.

D) £11,340.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The total flexible budgeted costs for 2011 are

A) £10,560.

B) £13,460.

C) £13,510.

D) £11,340.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

16

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget for total variable costs is

A) £90 U.

B) £180 U.

C) £790 F.

D) £880 F.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget for total variable costs is

A) £90 U.

B) £180 U.

C) £790 F.

D) £880 F.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is not an essential element of responsibility accounting?

A) assigning responsibility

B) establishing performance measures

C) evaluating performance

D) ridiculing poor performers

A) assigning responsibility

B) establishing performance measures

C) evaluating performance

D) ridiculing poor performers

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

18

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The static budget variance for rent is

A) £100 F.

B) £100 U.

C) £-0-.

D) £50 U.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The static budget variance for rent is

A) £100 F.

B) £100 U.

C) £-0-.

D) £50 U.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

19

Flexible budgets do NOT provide

A) expected costs for a range of activity.

B) budgeted costs for the actual level of activity.

C) budgeted costs for a predetermined level of activity.

D) expected costs for the actual performance level.

A) expected costs for a range of activity.

B) budgeted costs for the actual level of activity.

C) budgeted costs for a predetermined level of activity.

D) expected costs for the actual performance level.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

20

Figure 16-1

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data: The following actually occurred:

Refer to Figure 16-1. The flexible budget variance for supervision for 2011 is

A) £67 F.

B) £67 U.

C) £50 F.

D) none of these.

Armati, SA., is looking for feedback on company performance. The company compares the budget for the year with the actual costs. Data have been collected below:

Armati, SA., had the following budgeted data:

The following actually occurred: Refer to Figure 16-1. The flexible budget variance for supervision for 2011 is

A) £67 F.

B) £67 U.

C) £50 F.

D) none of these.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

21

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for purchasing in an activity-based performance report?

A) £1,000 U

B) £2,000 U

C) £3,000 U

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for purchasing in an activity-based performance report?

A) £1,000 U

B) £2,000 U

C) £3,000 U

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

22

Figure 16-4

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed: Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report:

Refer to Figure 16-4. What is the activity variance for design?

A) £40 F

B) £30 U

C) £15 F

D) £100 U

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed:

Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report: Refer to Figure 16-4. What is the activity variance for design?

A) £40 F

B) £30 U

C) £15 F

D) £100 U

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

23

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for inspection in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for inspection in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

24

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for maintenance in an activity-based performance report?

A) £50 F

B) £50 U

C) £550 U

D) £550 F

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for maintenance in an activity-based performance report?

A) £50 F

B) £50 U

C) £550 U

D) £550 F

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

25

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for maintenance in an activity-based performance report?

A) £1,000 U

B) £3,000 U

C) £3,000 F

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for maintenance in an activity-based performance report?

A) £1,000 U

B) £3,000 U

C) £3,000 F

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

26

An example of a negative incentive is

A) promotion.

B) nonfinancial incentive.

C) feedback reports.

D) termination of employment.

A) promotion.

B) nonfinancial incentive.

C) feedback reports.

D) termination of employment.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

27

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for machining in an activity-based performance report?

A) £1,000 U

B) £2,000 U

C) £3,000 U

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for machining in an activity-based performance report?

A) £1,000 U

B) £2,000 U

C) £3,000 U

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

28

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for machining in an activity-based performance report?

A) £50 F

B) £50 U

C) £800 U

D) none of the above

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for machining in an activity-based performance report?

A) £50 F

B) £50 U

C) £800 U

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

29

Figure 16-4

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed: Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report:

Refer to Figure 16-4. What is the actual cost of machining?

A) £24,970

B) £25,010

C) £25,050

D) none of the above

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed:

Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report: Refer to Figure 16-4. What is the actual cost of machining?

A) £24,970

B) £25,010

C) £25,050

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

30

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for total costs in an activity-based performance report?

A) £700 U

B) £700 F

C) £800 U

D) none of the above

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for total costs in an activity-based performance report?

A) £700 U

B) £700 F

C) £800 U

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

31

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for setups in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for setups in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following is NOT a key feature of an ideal budgetary system?

A) controllable costs

B) single measure for performance

C) incentives

D) frequent feedback

A) controllable costs

B) single measure for performance

C) incentives

D) frequent feedback

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

33

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for purchasing in an activity-based performance report?

A) £50 F

B) £50 U

C) £100 U

D) none of the above

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for purchasing in an activity-based performance report?

A) £50 F

B) £50 U

C) £100 U

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

34

Figure 16-4

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed: Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report:

Refer to Figure 16-4. What is the activity variance for purchasing?

A) £500 U

B) £100 U

C) £50 U

D) none of the above

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed:

Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report: Refer to Figure 16-4. What is the activity variance for purchasing?

A) £500 U

B) £100 U

C) £50 U

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

35

Figure 16-4

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed: Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report:

Refer to Figure 16-4. What is the actual cost of setups?

A) £160

B) £190

C) £300

D) none of the above

Villafane, SA., has done a cost analysis for its production of decals. The following activities and cost drivers have been developed:

Following are the actual costs of producing 35,000 decals: 1,000 machine hours; 5 batches; 30 purchase orders The following variances were given in the activity performance report: Refer to Figure 16-4. What is the actual cost of setups?

A) £160

B) £190

C) £300

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

36

Figure 16-2

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed: Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-2. What is the budget variance for total costs in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Glenn, SA., has done a cost analysis for its production of T-shirts. The following activities and cost drivers have been developed:

Following are the actual costs of producing 75,000 T-shirts: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-2. What is the budget variance for total costs in an activity-based performance report?

A) £1,000 F

B) £2,000 F

C) £3,000 F

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

37

Goal congruence means

A) there is alignment of organizational and managerial goals.

B) the organization is aligned to the needs of the environment.

C) the organization is aligned to shareholder goals.

D) there is no divergence between organization and stockholder goals.

A) there is alignment of organizational and managerial goals.

B) the organization is aligned to the needs of the environment.

C) the organization is aligned to shareholder goals.

D) there is no divergence between organization and stockholder goals.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

38

Figure 16-3

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed: Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders

Refer to Figure 16-3. What is the budget variance for setups in an activity-based performance report?

A) £50 F

B) £50 U

C) £800 U

D) none of the above

Harald, SA., has done a cost analysis for its production of bumper stickers. The following activities and cost drivers have been developed:

Following are the actual costs of producing 85,000 stickers: 5,000 machine hours; 10 batches; 20 purchase orders Refer to Figure 16-3. What is the budget variance for setups in an activity-based performance report?

A) £50 F

B) £50 U

C) £800 U

D) none of the above

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is NOT a key feature of an ideal budgetary system?

A) participation

B) incentives

C) accountability for noncontrollable costs

D) feedback on performance

A) participation

B) incentives

C) accountability for noncontrollable costs

D) feedback on performance

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following is NOT an advantage of participative budgeting?

A) encourages incrementalism

B) encourages communication

C) encourages responsibility

D) encourages creativity

A) encourages incrementalism

B) encourages communication

C) encourages responsibility

D) encourages creativity

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

41

Glock, SA., is looking for feedback on performance. The company compares the budget for the year with the actual costs.

Glock had the following budgeted data: Required:

Prepare a flexible budget for production costs for the following range of activity: 2,500 units; 4,000 units; 6,000 units.

Glock had the following budgeted data:

Required:Prepare a flexible budget for production costs for the following range of activity: 2,500 units; 4,000 units; 6,000 units.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

42

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. Which of the following describes the flexible budget variance for March?

A) The fixed overhead variance is £100 F.

B) The variable overhead variance is £1,000 U.

C) The variable overhead variance is £1,100 F.

D) both a and c

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Refer to Figure 16-5. Which of the following describes the flexible budget variance for March?

A) The fixed overhead variance is £100 F.

B) The variable overhead variance is £1,000 U.

C) The variable overhead variance is £1,100 F.

D) both a and c

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

43

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which of the following departments would NOT be classified as a profit centre?

A) the accounting department of a large PLc

B) the automotive division of a large PLc

C) the hardware department of a department store

D) the men's shoe department of a department store

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Which of the following departments would NOT be classified as a profit centre?

A) the accounting department of a large PLc

B) the automotive division of a large PLc

C) the hardware department of a department store

D) the men's shoe department of a department store

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

44

Which budget should be used to determine how efficiently managers controlled costs?

A) master budget

B) flexible budget

C) static budget

D) cash budget

A) master budget

B) flexible budget

C) static budget

D) cash budget

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

45

Controllable costs are those that a manager

A) has no authority over.

B) cannot avoid.

C) does not participate in authorizing.

D) can influence through decision making.

A) has no authority over.

B) cannot avoid.

C) does not participate in authorizing.

D) can influence through decision making.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

46

Figure 16-5

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Before implementing a responsibility accounting system, all areas of authority and responsibility within an organization must be clearly defined. Explain how this accomplished and why it is important.

Torino, SA., manufactures machine parts. Torino has developed a static budget for its plant at an activity level of 10,000 direct labour hours for the month of March. The actual level of activity was 11,000 hours. The following table summarizes the static budget and the actual costs for March:

Before implementing a responsibility accounting system, all areas of authority and responsibility within an organization must be clearly defined. Explain how this accomplished and why it is important.

Unlock Deck

Unlock for access to all 64 flashcards in this deck.

Unlock Deck

k this deck

47

Figure 16-5