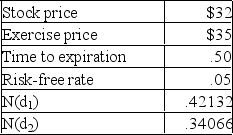

What is the value of a 6-month call with a strike price of $35 given the Black-Scholes Option Pricing Model and the following information?

A) $0

B) $0.13

C) $1.06

D) $1.85

E) $2.14

Correct Answer:

Verified

Q55: Three months ago,you purchased a put option

Q76: Three weeks ago,you purchased a July 45

Q125: A stock currently has a market value

Q126: A convertible bond has a face value

Q127: You own four call option contracts on

Q128: You sold one call option contract with

Q129: Underlying stock price: 45.80 Q131: You own a put option contract on Q132: You own six call option contracts on Q134: Kurt owns a convertible bond that matures![]()

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents