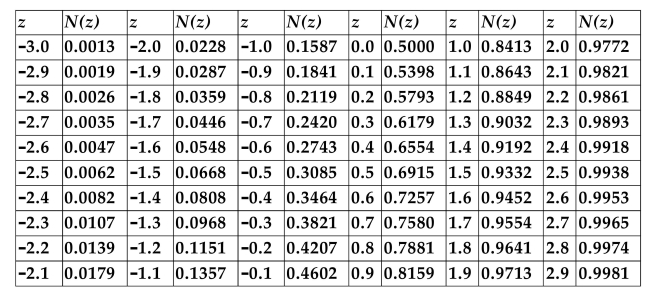

CUMULATIVE NORMAL DISTRIBUTION TABLE

-Refer to the information above. A stock is currently selling for $60. The stock pays no dividends. An American call option on the stock has a strike price of $55 and has 3 months to

Expiration. The standard deviation of the continuously compounded rate of return of the stock

Is 30%, and the annualized risk-free rate is 3%. Use the Black-Scholes formula to calculate the

Fair value of this option.

A) $7.66

B) $6.79

C) $7.03

D) The Black-Scholes formula cannot be used to determine the fair value of an American call option.

Correct Answer:

Verified

Q27: An investor can duplicate the payoffs generated

Q28: The volatility smile

A)suggests that the prices for

Q29: If there is to be no arbitrage

Q30: A European call option on a stock

Q31: An investor buys a call with a

Q33: The value of the right to exercise

Q34: What is the difference between writing a

Q35: A European call option on a stock

Q36: Which of the following values can not

Q37: CUMULATIVE NORMAL DISTRIBUTION TABLE ![]()

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents